International Development Association

Management’s Discussion & Analysis

and

Financial Statements

June 30, 2022

Contents

Section I: Executive Summary

Section II: Overview

Section IV: Financial Results

Section V: Development Activities, Products

and Programs

Section VI: Other Development Activities and

Programs

Section VII: Investment Activities

Section VIII: Borrowing Activities

Section IX: Risk Management

Section X: Critical Accounting Policies and the

Use of Estimates

Section XI: Governance and Internal Controls

Appendix

Summary of Financial Results 4

Presentation 6

Introduction 6

Twentieth Replenishment of Resources (IDA20) 6

Financial Business Model 6

Basis of Reporting 7

IDA19 Funding 8

IDA20 Funding 9

Allocation of IDA20 Resources 9

Financial Results and Portfolio Performance 15

Lending Framework 24

Financial Terms 25

Loans, Grants and Guarantee Activity 27

Guarantees 29

Other Financial Products and Services 30

Grant Making Facilities 30

Debt Relief 30

Externally-Funded Activities 30

Investments Trading Portfolio 33

Investments - Non-Trading Portfolio 34

Concessional Partner Loans 35

Market Debt 35

Other Short-Term Borrowings 36

Contractual Obligations 36

Risk Governance 37

Risk Oversight and Coverage 37

39

Fair Value of Financial Instruments 49

Provision for Losses on Loans and Other Exposures 49

Provision for HIPC Debt Initiative and MDRI 49

Business Conduct 50

General Governance 50

Audit Committee 51

External Auditors 52

Senior Management Changes 52

Internal Controls 52

Glossary of Terms 53

List of Tables, Figures and Boxes 54

Section I: Executive Summary

2 June 30, 2022

This Management’s Discussion & Analysis (MD&A) discusses the results of the International Development

Association’s (IDA) financial performance for the fiscal year ended June 30, 2022 (FY22). IDA undertakes no

obligation to update any forward-looking statements. Certain reclassifications of prior years’ information have been

made to conform with the current year’s presentation. For discussion of IDA’s financial results for the year ended

June 30, 2021, as compared to the year ended June 30, 2020, see Section IV – Financial Results in IDA’s MD&A and

Financial Statements for the fiscal year ended June 30, 2021 (FY21). For information relating to IDA’s development

operations’ results and corporate performance, refer to the World Bank Corporate Scorecard and Sustainability

Review.

Box 1: Selected Financial Data

In millions of U.S. dollars, except ratios which are in percentages

As of and for the fiscal years ended June 30,

2022

2021

2020

Lending Highlights (Sections IV & V)

Loans, Grants and Guarantees

Net commitments

a

$

37,727

$

36,028

$

30,365

Gross disbursements

a

21,214

22,921

21,179

Net disbursements

a

14,477

16,465

15,112

Balance Sheet (Section IV)

Total assets

$

220,014

$

219,324

$

199,472

Net investment portfolio

b

39,561

37,921

35,571

Net loans outstanding

174,490

177,779

160,961

Borrowing portfolio

c

35,032

28,335

19,653

Total equity

178,668

180,876

168,171

Income Statement (Section IV)

Interest revenue, net of borrowing expenses

$

1,901

$

1,996

$

1,843

Transfers from affiliated organizations and others

274

544

252

Development grants

(2,372)

(2,830)

(1,475)

Net income (loss)

12

(433)

(1,114)

Non-GAAP Measures:

Adjusted Net Income (Section IV)

$

260

$

394

$

724

Deployable Strategic Capital Ratio (Section IX)

26.4%

30.4%

35.8%

a. Commitments that have been approved by the Executive Directors (referred to as “the Board” in this document) and are net of full

cancellations / terminations approved in the same fiscal year. Commitments and disbursements exclude IDA-IFC-MIGA Private

Sector Window (PSW) activities.

b. For composition of the net investment portfolio, see Notes to the Financial Statements, Note C – Investments – Table C2.

c. Includes associated derivatives.

Section I: Executive Summary

June 30, 2022 3

Section I: Executive Summary

IDA, an international organization owned by its 174

1

member countries, is one of the five institutions of the World

Bank Group (WBG

2

). Each WBG organization is legally and financially independent from IDA, with separate assets

and liabilities. IDA is not liable for the obligations of the other institutions.

IDA is rated triple-A by the major rating agencies and has been providing financing and knowledge services to many

of the world’s developing countries for more than 61 years. With its many years of experience and its depth of

knowledge in the international development arena, IDA plays a key role in achieving the WBG’s goal of helping

countries achieve better development outcomes. IDA contributes to the WBG’s twin goals of ending extreme poverty

and promoting shared prosperity by providing loans, grants, and guarantees, and other financial products to the poorest

and most vulnerable countries to help meet their development needs and by providing technical assistance and policy

advice leveraging its experience and expertise. It also supports countries with disaster risk financing and insurance

against natural disasters and health related crises and facilitates financing through trust fund partnerships.

IDA and its affiliated organizations seek to help countries achieve improvements in growth, job creation, poverty

reduction, governance, the environment, climate adaptation and resilience, human capital, infrastructure, and debt

transparency, among others. To meet its development goals, the WBG has been increasing its focus on country

programs in order to improve growth and development outcomes. Further, the last fiscal year brought new challenges

to the global outlook – high inflation and the rise in food insecurity that came on top of growing inequality, global

fragility, the coronavirus disease (COVID-19) pandemic and other geopolitical events, rising debt, and

macroeconomic imbalances. In response, IDA, as part of the WBG efforts, continues to work with partners at global

and country levels to support its borrowing countries in addressing the impact of these multiple crises, to enhance

resilience, and lay the groundwork for rebuilding better. The responses all remain in compliance with IDA’s existing

financial, operational and risk management policies.

The nineteenth replenishment of IDA (IDA19), which ended in FY22, built on the strong momentum of the IDA18

financing framework by combining contributions from members with market borrowings. IDA’s hybrid financial

model has allowed IDA to significantly expand its financial capacity and provide $72 billion in financing for its clients

from the IDA19 replenishment.

On March 31, 2022, IDA’s Twentieth Replenishment (IDA20) was approved by the Board of Governors. In April

2021, members agreed to launch IDA20 one year early, to commence in FY23, and to shorten IDA’s Nineteenth

Replenishment (IDA19) implementation period to two years (FY21-FY22). The IDA20 operational and financing

framework will continue to leverage IDA’s strong equity base to help low-income countries respond to the COVID-

19 crisis and build a greener, more resilient, and inclusive future. Members agreed to a financing envelope of $93

billion

3

over the three-year replenishment period, FY23-FY25, supported by $23.5 billion of member contributions.

See Section III: IDA’s Financial Resources.

1

On November 3, 2021, Bulgaria became the 174

th

member country of IDA.

2

The other WBG institutions are the International Bank for Reconstruction and Development (IBRD), the International Finance

Corporation (IFC), the Multilateral Investment Guarantee Agency (MIGA), and the International Centre for Settlement of Investment

Disputes (ICSID). The World Bank consists of IBRD and IDA.

3

U.S. dollar amounts are based on IDA20 reference rate of USD/SDR 1.42934. The U.S. dollar amounts are provided for reporting

purposes only, as IDA’s balance sheet is predominantly managed in Special Drawing Rights (SDR).

Section I: Executive Summary

4 June 30, 2022

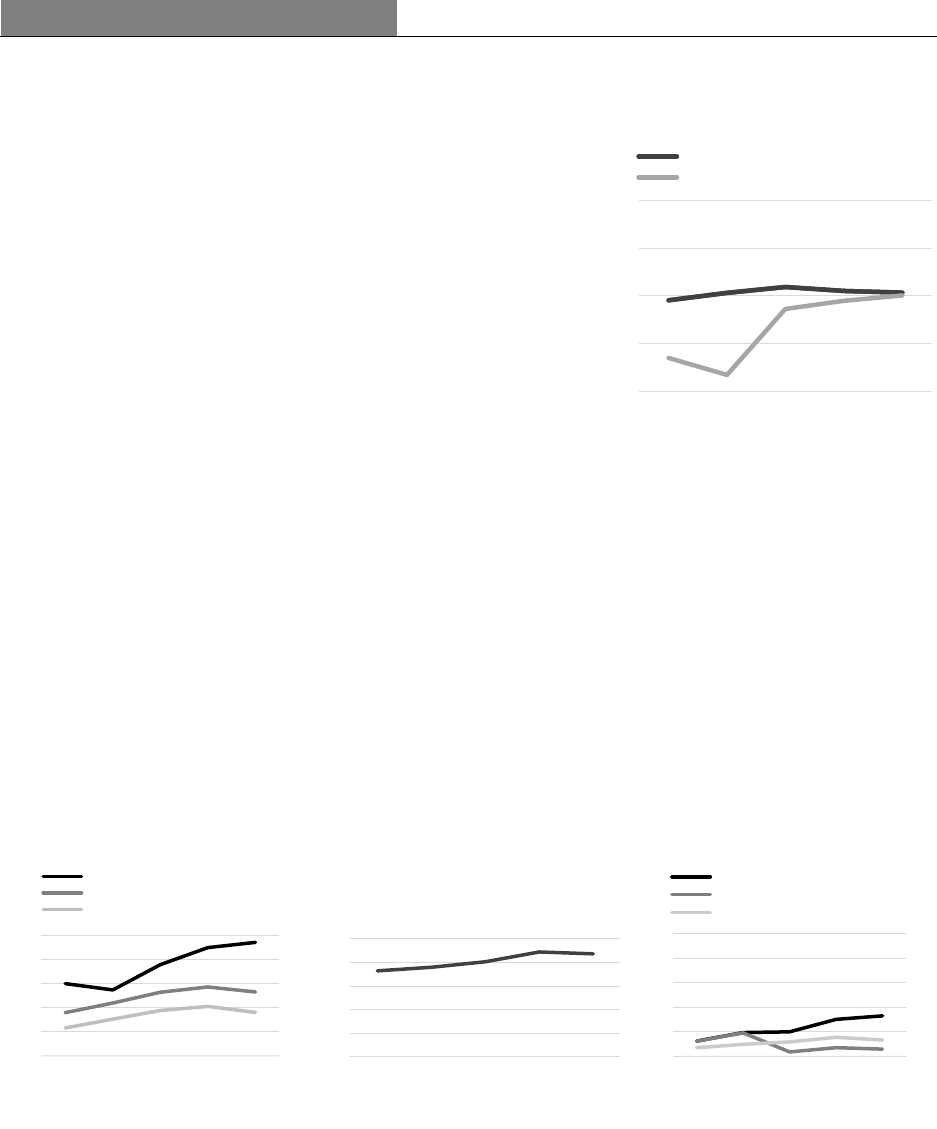

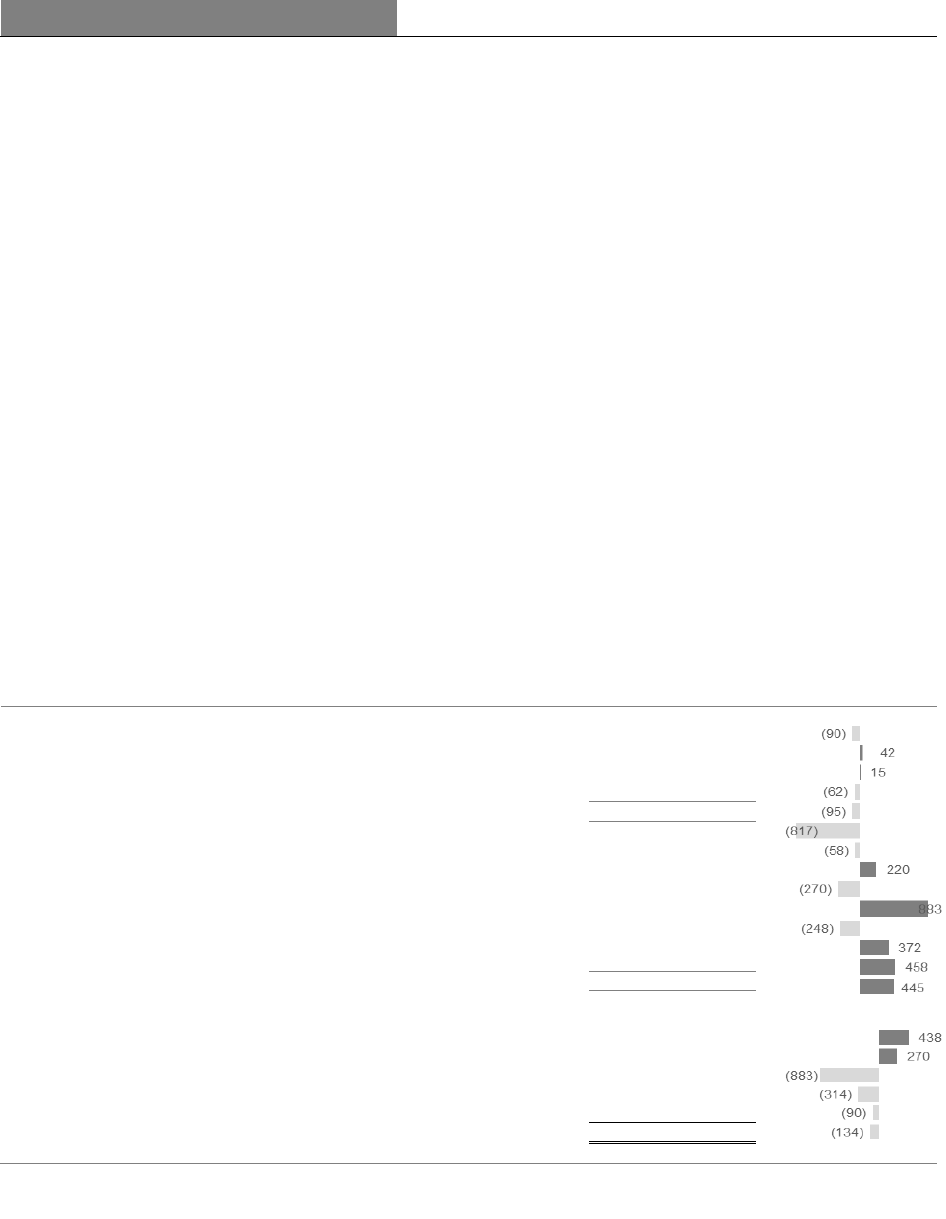

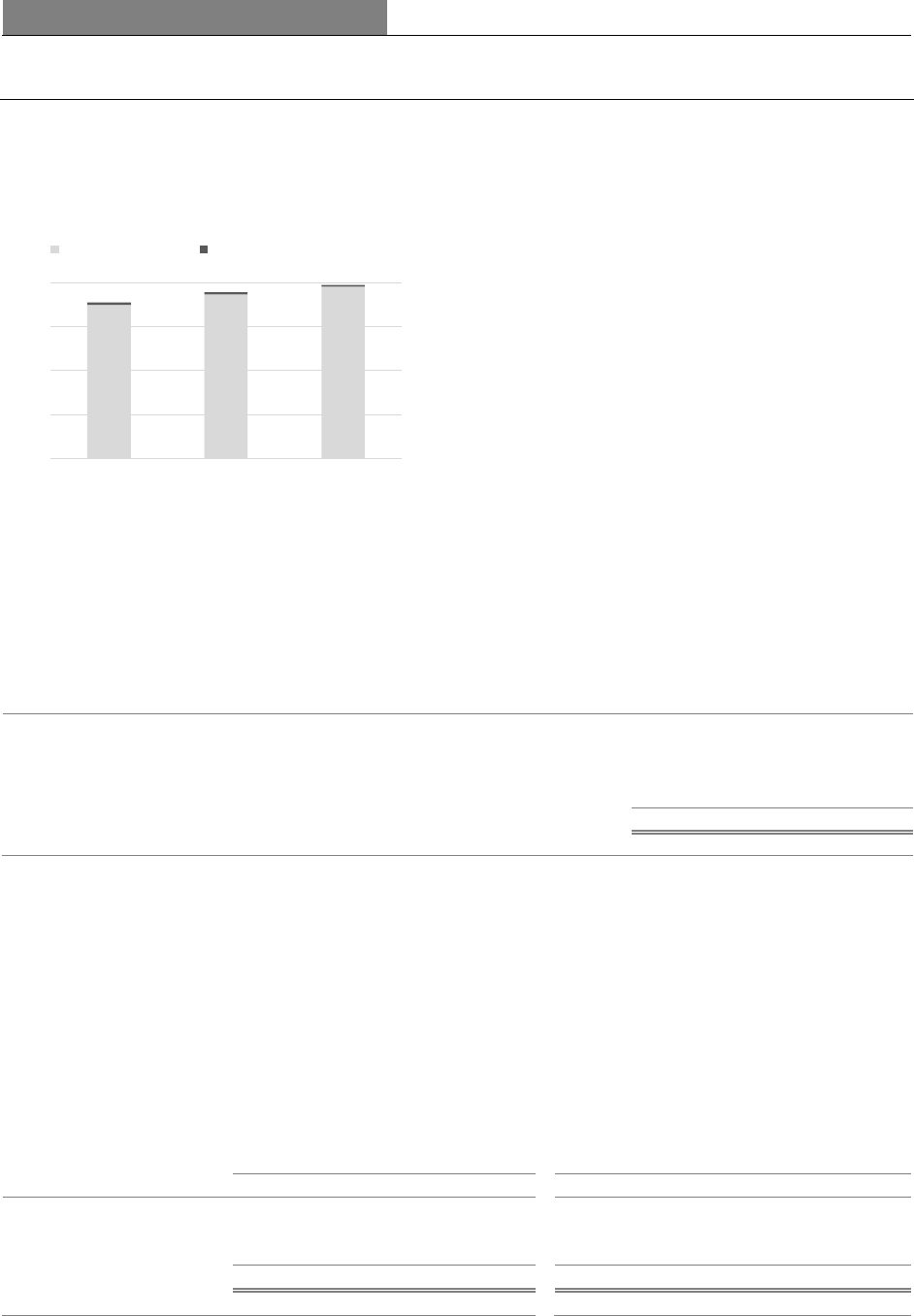

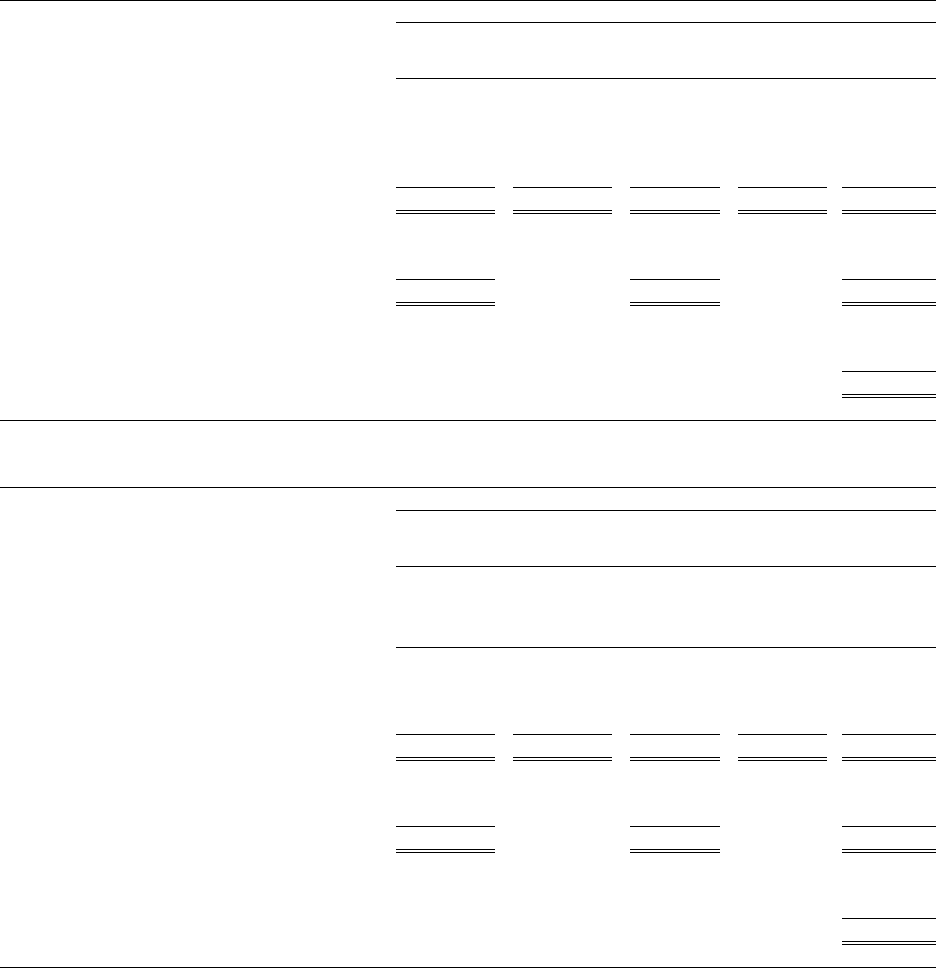

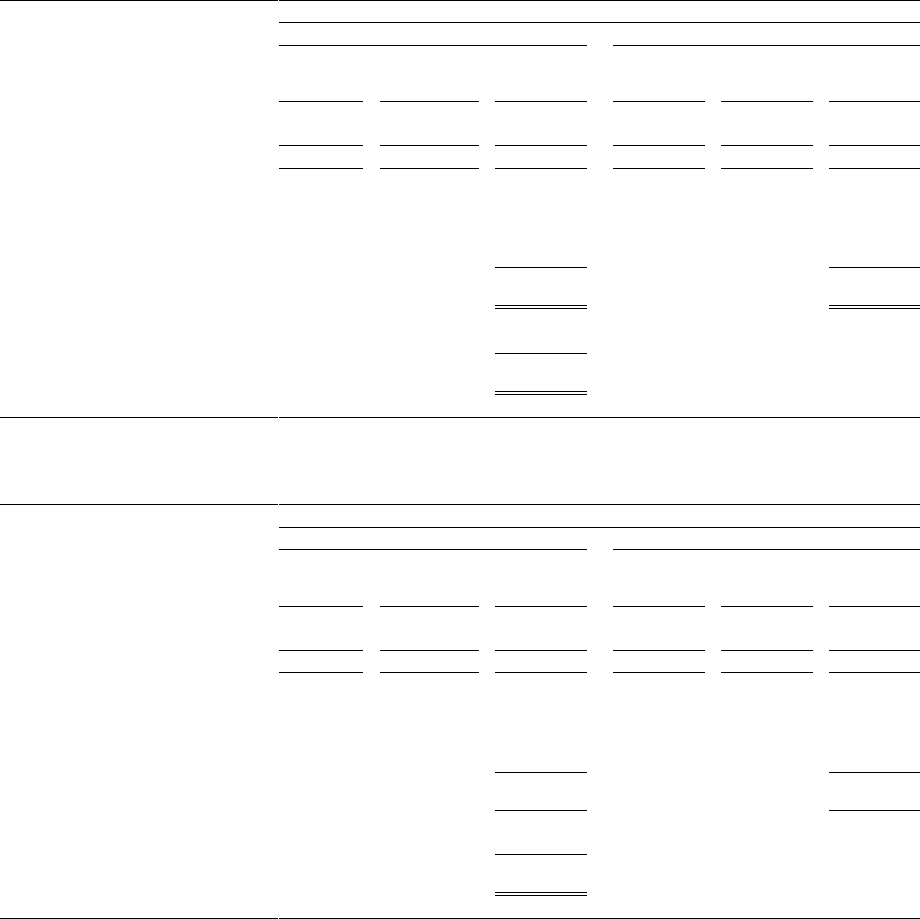

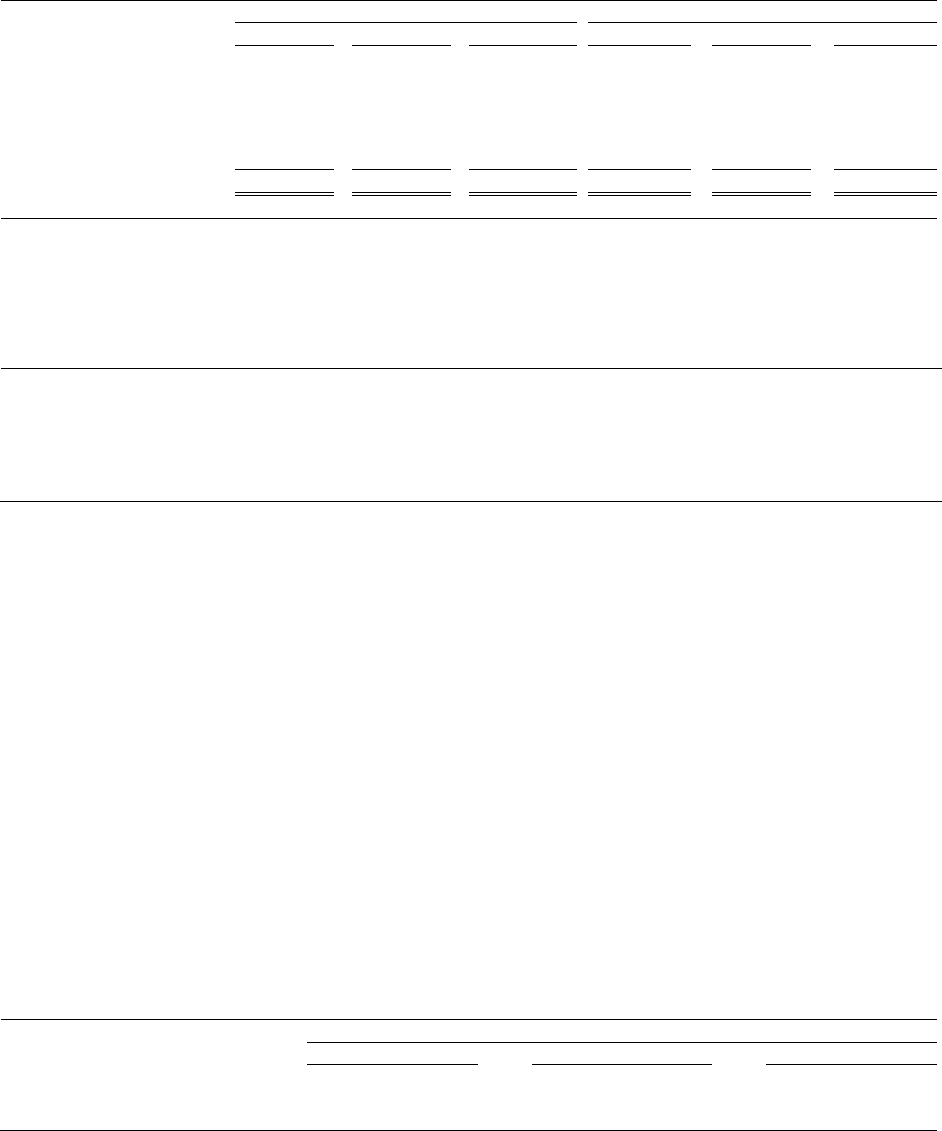

Summary of Financial Results

Net Income and Adjusted Net Income

Net Income: IDA reported net income of $12 million in FY22,

compared to a net loss of $433 million in FY21. The increase was

primarily driven by non-functional currency translation adjustments

and the decrease in development grant expenses, partially offset by

the increase in the provision for losses on loans and other exposures.

See Section IV: Financial Results.

Adjusted Net Income: IDA’s adjusted net income was $260 million

in FY22, compared to $394 million in FY21. The decrease was

primarily due to lower interest revenue on loans and higher net non-

interest expenses. See Section IV: Financial Results.

In millions of U.S. dollars

Lending Operations

IDA’s net commitments in FY22 were $37.7 billion, 5% higher than FY21 and the highest annual level in IDA’s

history. Out of the total net commitments, $24.5 billion were loan commitments and $13.2 billion were grant

commitments. FY22 commitments reflected continued support for COVID-19 related efforts, including $2.3 billion

of financing for COVID-19 vaccines and $3.7 billion of financing for food security. In addition, FY22 commitments

included $1 billion financing to provide fast-disbursing support for Ukraine on an exceptional basis.

IDA’s net loans outstanding decreased by $3.3 billion, from $177.8 billion as of June 30, 2021, to $174.5 billion as

of June 30, 2022, primarily due to currency translation losses as the SDR depreciated against the U.S. dollar, partially

offset by net loan disbursements during the year. See Section IV: Financial Results.

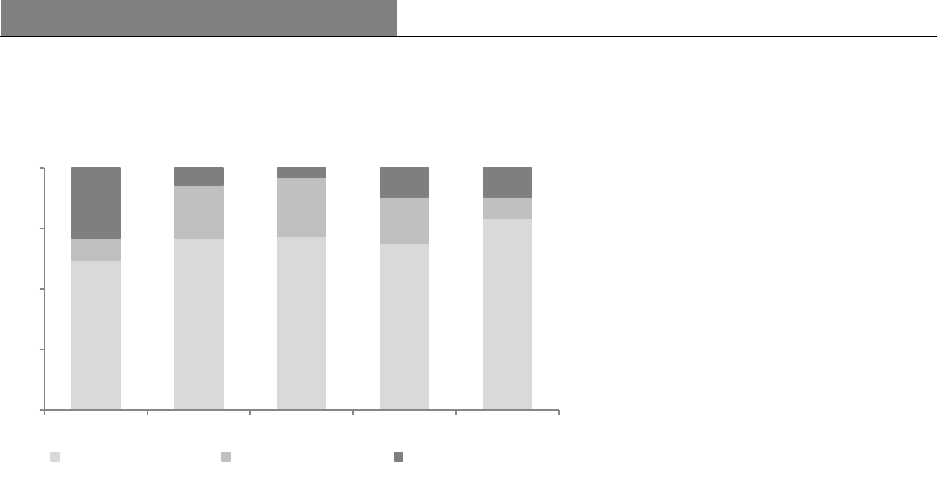

Development grant expenses were $2.4 billion in FY22 compared to $2.8 billion in FY21. The development grant

activity volume in FY22 was higher than FY21, excluding grants of $1.3 billion disbursed to Sudan in the previous

year after its arrears were cleared in March 2021. The decrease in development grant expenses from FY19 to FY20,

as shown in the graph below, is due to the timing of the recognition of the grant expenses as a result of the

implementation of a new accounting standard in FY20.

In billions of U.S. dollars

a. Includes loans, grants, and guarantees.

(8,000)

(4,000)

0

4,000

8,000

FY18 FY19 FY20 FY21 FY22

Adjusted Net Income (Loss)

Net Income (Loss)

0

8

16

24

32

40

FY18 FY19 FY20 FY21 FY22

Net Commitments

Gross Disbursements

Net Disbursements

0

40

80

120

160

200

Jun 18 Jun 19 Jun 20 Jun 21 Jun 22

Net Loans Outstanding

0

8

16

24

32

40

FY18 FY19 FY20 FY21 FY22

Net Grant Commitments

Grant Expense

Net Grant Disbursements

a

Section I: Executive Summary

June 30, 2022 5

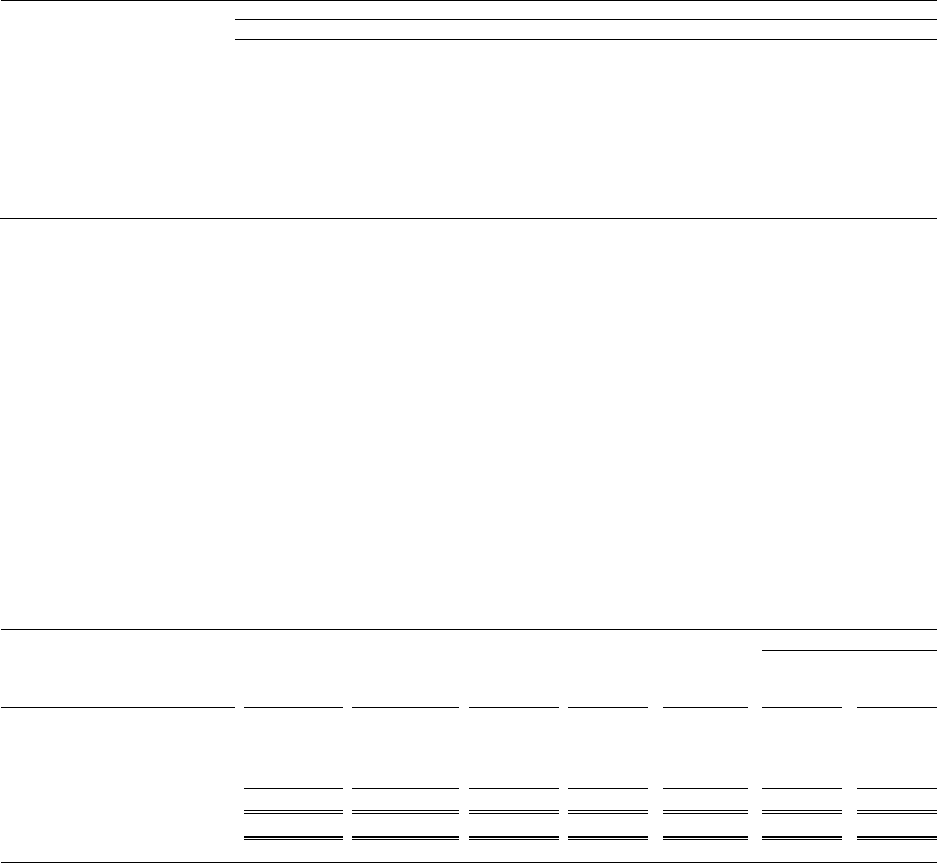

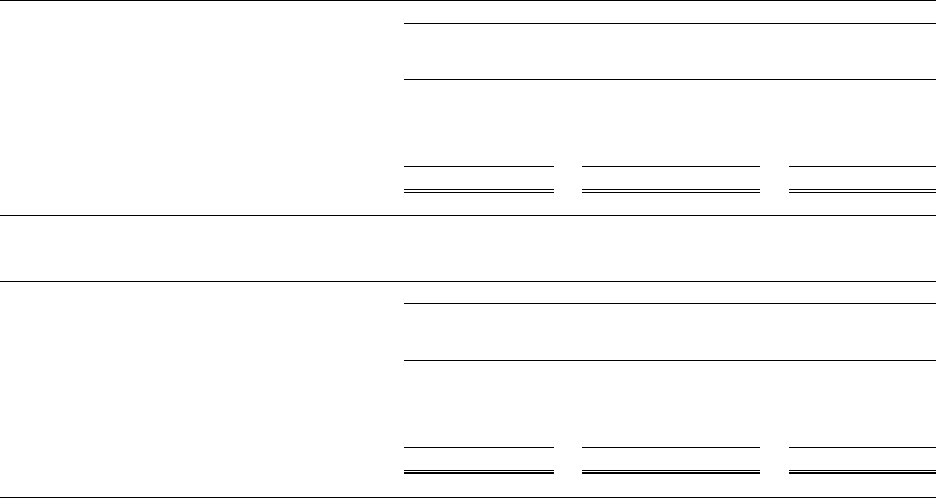

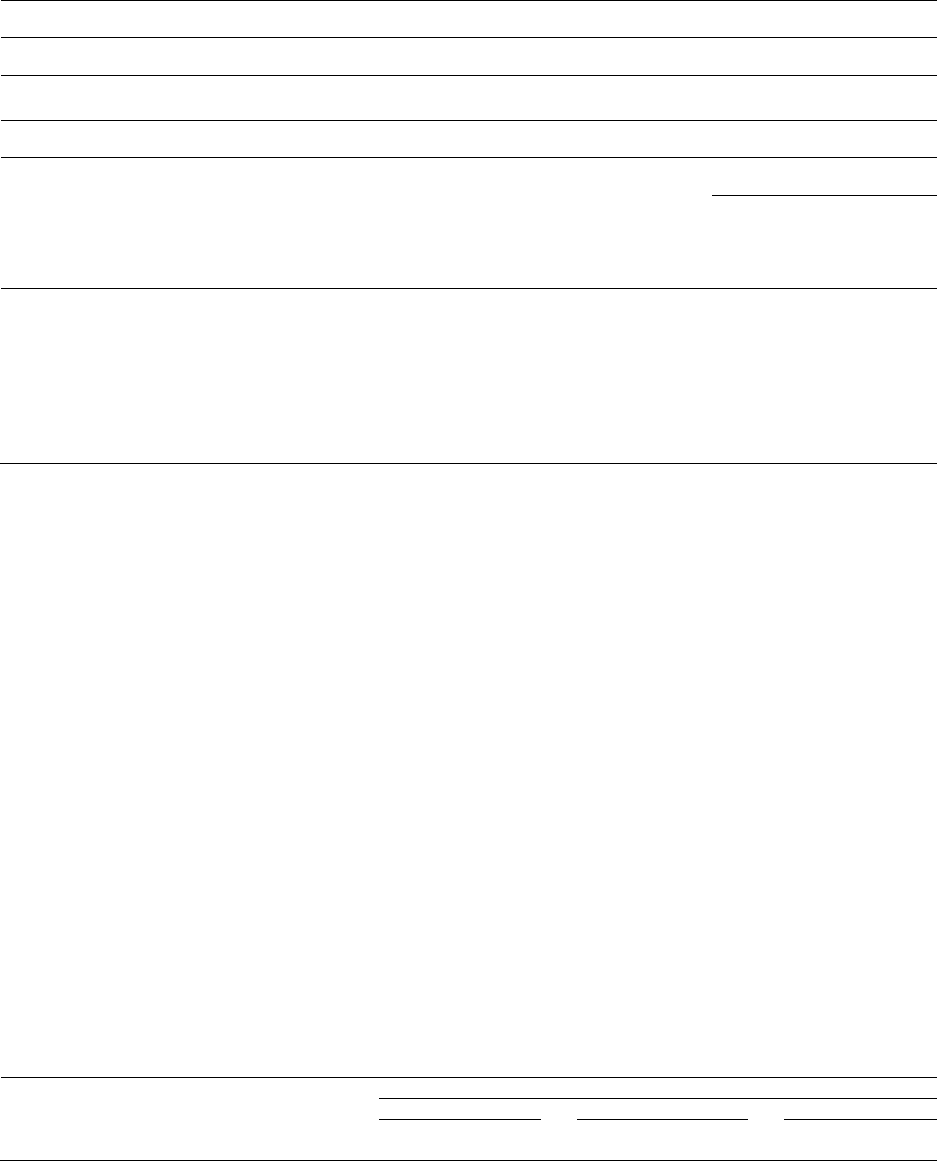

Net Investment Portfolio

As of June 30, 2022, the net investment portfolio was $39.6 billion,

compared with $37.9 billion as of June 30, 2021. See Section VII:

Investment Activities. The primary objective of IDA’s investment

strategy is principal protection. As of June 30, 2022, 74% of IDA’s

investment portfolio was held in instruments rated AA or above (See

Table 30).

In billions of U.S. dollars

Borrowing Portfolio

Market borrowings at fair value: As of June 30, 2022, the market

borrowings carried at fair value, and the related derivatives were

$21.9 billion, an increase of $1.3 billion from June 30, 2021.

Market borrowings at amortized cost: As of June 30, 2022, the

market borrowings carried at amortized cost were $6.2 billion (Nil -

June 30, 2021).

Concessional Partner Loans at amortized cost: As of June 30,

2022, total borrowings from members - Concessional Partner Loans

(CPL) were $7.0 billion, a decrease of $0.7 billion from June 30,

2021.

In billions of U.S. dollars

Equity and Capital Adequacy

As of June 30, 2022, IDA’s equity was $178.7 billion, a decrease of

$2.2 billion from June 30, 2021. The decrease was primarily due to

currency translation losses consistent with the depreciation of the

SDR against the U.S. dollar. See Section IV: Financial Results.

In billions of U.S. dollars

The Deployable Strategic Capital (DSC) ratio, IDA’s main capital

adequacy measure, was 26.4% as of June 30, 2022, above the zero

percent policy minimum and a decrease of 4.0 percentage points

from 30.4% as of June 30, 2021. IDA’s capital continues to be

adequate to support its operations. See Section IX: Risk

Management.

Ratio in percentages

0

10

20

30

40

50

Jun 18 Jun 19 Jun 20 Jun 21 Jun 22

Net Investment Portfolio

0

10

20

30

40

50

Jun 18 Jun 19 Jun 20 Jun 21 Jun 22

Borrowing portfolio

0

50

100

150

200

Jun 18 Jun 19 Jun 20 Jun 21 Jun 22

Equity

Policy Minimum Ratio = 0%

0%

15%

30%

45%

Jun 18 Jun 19 Jun 20 Jun 21 Jun 22

Deployable Strategic Capital Ratio

Section II: Overview

6 June 30, 2022

Section II: Overview

Presentation

This document provides Management’s Discussion and Analysis of the financial condition and results of operations

for IDA for the fiscal year ended June 30, 2022. A Glossary of Terms is provided at the end of this document.

Introduction

Generally, every three years, representatives of IDA’s members

4

meet to assess IDA’s financial capacity and the

medium-term demand for new IDA financing. Members decide on the policy framework, agree upon the amount of

financing to be made available for the replenishment period, and commit to additional contributions of equity that are

required to meet these goals. The meetings culminate in a replenishment agreement that determines the size, sources

(both internal and external), and uses of funds for the replenishment period.

Twentieth Replenishment of Resources (IDA20)

On March 31, 2022, the IDA20 Resolution was approved by IDA’s Board of Governors. IDA20 recognizes the need

to help address the profound challenges faced by IDA countries. IDA20 reaffirms the international community’s

commitment to scale up support to enable IDA countries to respond to the effects of the COVID-19 crisis, recoup their

development losses, and resume progress toward the 2030 Sustainable Development goals. IDA20 will support the

world’s poorest and most vulnerable countries to emerge on a development path in line with the Green, Resilient and

Inclusive Development (GRID) framework. IDA20 will build on the IDA19 special themes, with the continuation of

human capital, climate change, fragility, conflict, and violence (FCV), gender and development, jobs, and economic

transformation. In addition, IDA20’s policy package will incorporate four crosscutting issues: crisis preparedness,

governance and institutions, debt (including transparency), and technology.

With this agenda in the forefront, IDA members agreed on the IDA20 operational and financing framework that

reflects a financing envelope of $93 billion, over a three-year replenishment period (FY23-FY25), that will be

supported by $23.5 billion of member contributions. The remainder of the financing envelope will be covered by the

Multilateral Debt Relief Initiative (MDRI), financing raised in the capital markets, the IDA19 carry-over, internal

resources (e.g., loan repayments) and transfers from IBRD.

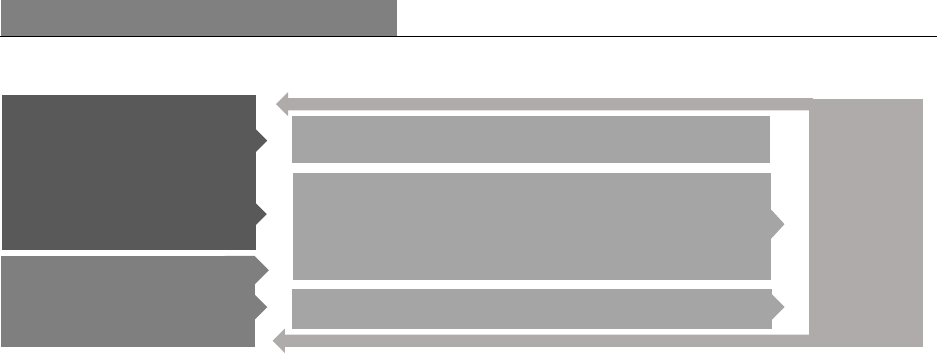

Financial Business Model

IDA has financed its operations over the years with its own equity, including regular additions to equity provided by

member countries as part of the replenishment process. As a result of the strong support of member countries, IDA

has built up a substantial equity base of $178.7 billion as of June 30, 2022. In FY15, IDA introduced debt to its

financial model with concessional partner loans received from certain member countries. In FY18, IDA introduced a

hybrid financing model by including market debt into its business model. By prudently leveraging its equity and

blending market debt with equity contributions from members, IDA has increased its financial efficiency, and scaled

up its financing to support the escalating demand for its resources to deliver on the following priorities:

• Provide concessional financing on terms that respond to clients’ needs; and

• Ensure long-term financial sustainability of IDA’s financial model through a prudent risk management framework.

Non-concessional lending will primarily be financed by market debt. Concessional lending, including grants, is

primarily financed by IDA’s equity. As IDA’s funding program expands under the hybrid financing model, a bigger

portion of concessional lending will be funded by market debt, together with member countries’ contributions (equity).

Funds not deployed for lending are maintained in IDA’s investment portfolio to supply liquidity for its operations.

See Figure 1.

4

IDA’s members are owners and hold voting rights in IDA. Members do not, however, hold shares in IDA and are therefore not

referred to as shareholders. Payments for subscriptions and contributions from members increase IDA’s paid-in equity and are

financially equivalent to paid-in capital in multilateral development organizations that issue shares.

Section II: Overview

June 30, 2022 7

Figure 1: IDA's Financial Business Model

Basis of Reporting

IDA prepares its financial statements in conformity with accounting principles generally accepted in the United States

of America (U.S. GAAP). IDA’s functional currencies are the SDR and its component currencies of the U.S. dollar,

euro, Japanese yen, pound sterling and Chinese renminbi and IDA’s reporting currency is the U.S. dollar. Management

uses net income as the basis for deriving adjusted net income, as discussed in Section IV: Financial Results.

Adjusted Net Income

Adjusted Net Income (ANI), a non-GAAP measure, reflects the economic results of IDA’s operations and is used by

IDA’s management and the Board as a financial sustainability measure. ANI is defined as IDA’s net income, adjusted

to exclude certain items. After the effects of these adjustments, the resulting ANI generally reflects amounts which

are realized, not restricted for specific uses, and not directly funded by members. For a detailed discussion of the

adjustments, see Section IV: Financial Results.

Non Concessional Lending

Concessional Lending and Investments

Grants

Reflows and Operating

Results

Borrowings

Equity

8 June 30, 2022

Financial Resources

IDA’s replenishments have grown from $1.0 billion in the initial replenishment to $93 billion in IDA20. Members’

subscriptions and contributions receivable for each replenishment are settled through payment of cash or deposit of

nonnegotiable, non-interest-bearing demand notes which become due throughout the replenishment period, generally

three years. The notes are encashed by IDA on a pro rata basis over a 9 to 11-year period which generally corresponds

with the disbursement period of the loans and grants.

IDA19 Funding

In April 2021, the IDA19 financing period was shortened to two years (FY21-FY22) and the IDA19 financing

framework was adjusted to $71 billion from the original commitment authority of $82 billion. The remaining $11

billion was carried forward to be utilized in the replenishment period of IDA20. In April 2022, IDA’s Board approved

an increase in the adjusted IDA19 commitment authority by $1 billion to $72 billion to support the urgent development

financing needs and to supplement IBRD and development partners’ support for Ukraine. The increase did not impact

the use of the original IDA19 financing plan of $71 billion.

As of June 30, 2022, IDA completed its nineteenth replenishment period. See Table 1 for results for IDA19 sources

and uses.

Table 1: Results for IDA19 Sources and Uses

In billions of U. S. dollars

Sources

USD equivalent

a

Member equity contributions

$

23.5

Member compensation for MDRI

3.9

Reflows, carryover, and borrowings

54.7

Transfers from IBRD

0.9

Total Sources

$

83.0

Uses

USD equivalent

b

Concessional financing

Loans and guarantees

c

$

45.1

Grants

25.4

Non-concessional financing

4.5

Private Sector Window

1.7

Less: Recommitments of cancellations from previous replenishments

(4.7)

Total Uses

$

72.0

Carry-over to IDA20

$

11.0

Total Uses and Carry-over

$

83.0

a. U.S. dollar amounts are based on IDA19 reference rate of USD/SDR 1.38318. The U.S. dollar amounts are provided for reporting

purposes only.

b. U.S. dollar amounts are based on exchange rate as per the date of approval.

c. Includes $1.2 billion of loans approved by the Board in July 2022 due to the extension of the closing date for the approval of

IDA19 operations.

Figure 2 below shows the allocation of IDA19 sources to fund IDA’s lending activities (excluding PSW activities).

Figure 2: Funding Allocation during IDA19 replenishment period

Regular loans

23%

Blend loans

37%

Grants

34%

Non-concessional

6%

June 30, 2022 9

Table 2: Cumulative Net Commitments during the IDA19 replenishment period

In millions of U.S. dollars

As of June 30, 2022

Loans and

Guarantees

Grants

Total

Concessional financing

IDA Country Allocations

$

39,382

$

19,576

$

58,958

IDA Concessional Windows

Regional Window

3,447

2,450

5,897

Window for Host Communities and Refugees

30

1,239

1,269

Crisis Response Window

1,024

1,089

2,113

Arrears Clearance

-

1,000

1,000

Non-concessional financing

4,518

-

4,518

Total Net Commitments

a

$

48,401

$

25,354

$

73,755

a. Commitments are net of full cancellations/terminations approved in the same fiscal year. Commitments exclude IDA-IFC-MIGA

Private Sector Window (PSW) activities of $1.7 billion, and $1.2 billion of loans approved by the Board in July 2022 associated with

IDA19.

IDA20 Funding

IDA’s financing resource envelope available for lending and grant commitments is based on the long-term outlook of

IDA’s financial sustainability. This takes into account the amount of member contributions and the concessionality of

the proposed financing to borrowers, market conditions, and capital adequacy requirements.

Allocation of IDA20 Resources

Eligibility for IDA’s resources is determined primarily by a member’s relative poverty. Relative poverty is defined as

Gross National Income (GNI) per capita below an established threshold and is updated annually. For FY23, the

threshold is $1,255 (FY22: $1,205).

Table 3: IDA20 Sources and allocation

In billions of U.S dollars

Sources

USD equivalent

a

Member equity contributions

$

23.5

Member compensation for MDRI

1.8

Reflows, carryover, and borrowings

66.9

Transfers from IBRD

0.8

Total Sources

$

93.0

Allocation

USD equivalent

a

Concessional financing

Country Allocation Envelope

$

62.8

IDA Concessional Windows

21.4

Non-concessional financing

6.3

Private Sector Window

2.5

Total Allocation

$

93.0

a. U.S. dollar amounts are based on IDA20 reference rate of USD/SDR 1.42934. The U.S. dollar amounts are provided for reporting

purposes only.

10 June 30, 2022

As of July 1, 2022, 74 countries are eligible to borrow from IDA on concessional terms as follows:

IDA eligible

countries

IDA-only

40 countries that (a) have not exceeded the IDA operational cut-off GNI per capita for

more than two consecutive years; and (b) are not creditworthy to borrow from IBRD.

This includes: 11 Small Island Economies that have per capita incomes above the IDA

operational cut-off for more than two consecutive years, but that have been granted

-.

2 countries with loans in nonaccrual status, which were -o

time they became nonaccrual countries.

Gap

17 countries that are (a) determined by IDA to be eligible for IDA financing; (b)

determined by IDA to have a GNI per capita that has exceeded the cut-off for IDA

eligibility for more than two consecutive years; and (c) not currently determined by

IBRD to be creditworthy to borrow from IBRD. This includes 3 Small States that are

not island states.

Blend

14 countries that are determined: (a) by IDA to be eligible for IDA financing; and (b)

by IBRD to be creditworthy to borrow from IBRD. This includes 6 Small Island

Economies and 1 Small State that is not an island state.

1

it became a nonaccrual country.

IDA financing is provided in the form of loans, grants, and guarantees. Most of IDA’s resources are allocated to

eligible members through IDA Country Allocations that provide unearmarked support. IDA Country Allocations are

determined using the Performance Based Allocation (PBA) system, which takes into account the country’s

performance rating (CPR), population size and per capita income, and complemented by the FCV envelope. The rest

of IDA resources are provided through five IDA Windows dedicated to addressing specific development priorities,

and an Arrears Clearance framework that provides exceptional support for countries to fully reengage with the World

Bank. The allocation framework is agreed for each replenishment cycle.

Figure 3: Allocation of IDA20 Resources

Allocation - Performance Based Allocation (PBA) System

IDA’s resources are allocated to eligible members, using its PBA system and the allocation framework agreed during

each replenishment. These allocations depend on several factors: the overall availability of IDA’s resources, individual

country needs, their policy performance and institutional capacity, and each country’s performance relative to others.

The PBA system is designed to provide resources where they are likely to be most helpful in reducing poverty.

Under the PBA, the main factor that determines the allocation of IDA’s core concessional resources among eligible

countries is their performance in the Country Policy and Institutional Assessment (CPIA). The CPIA reflects the

results of an exercise that rates eligible countries against a set of criteria including economic management; structural

policies; policies for social inclusion and equity; and public-sector management and institutions. The CPIA and

portfolio performance together constitute the IDA Country Performance Rating (CPR). In addition to the CPR,

population, and per capita income are factored into a country’s allocation, along with the annual base allocation

(SDR15 million per country). In addition, country allocations provide the FCV envelope to enhance support for

eligible countries facing different FCV risks. The Sustainable Development Finance Policy (SDFP), which became

effective at the beginning of IDA19, aims to incentivize IDA-eligible countries to move towards transparent,

sustainable financing and to promote coordination between IDA and other creditors in support of these countries’

June 30, 2022 11

efforts to address their debt-related vulnerabilities. A set-aside from or a discount of IDA’s country allocation are used

to incentivize satisfactory implementation of Performance and Policy Actions. Countries which demonstrate

satisfactory progress in implementing their Performance and Policy Actions have access to their full annual country

allocation. Countries that do not satisfactorily implement their Performance and Policy Actions will either have a

share of their country allocation set aside or their country allocation will be reduced.

In recognition of the change in IDA’s business model starting in IDA18, and to ensure that its lending decisions are

compatible with the capital adequacy requirements of a triple-A rating, the allocation framework for IDA20 continues

to be aligned with the Single Borrower Limit (SBL) and capital adequacy requirements under the DSC Framework,

see Section IX: Risk Management.

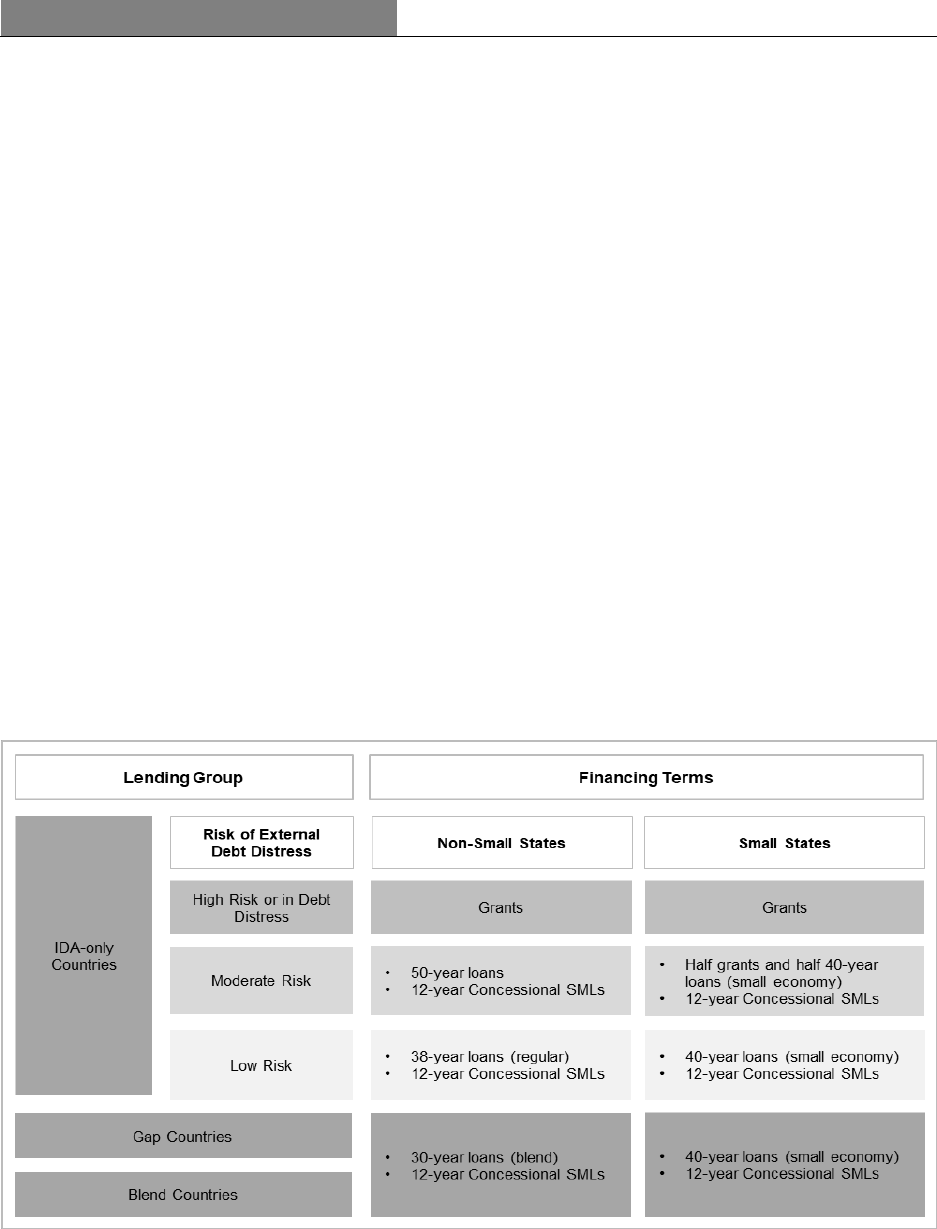

Concessional Financing

Concessional financing is provided in the form of loans, grants and guarantees. Eligibility and percentage of allocation

for grants for IDA-only countries are based on an assessment of the country’s risk of debt distress, where countries

with high risk of debt distress will receive their IDA assistance in grants. Gap and Blend countries are only eligible

for grant financing via the Window for Host Communities and Refugees, if applicable.

As part of IDA’s balance sheet optimization measures, new financing terms have been introduced in IDA20 which

include:

• Concessional Shorter-Maturity Loans (SMLs). Concessional SMLs will be offered through the Scale-Up Window

(SUW) and country allocations based on the PBA system. IDA-only countries at moderate and low risk of debt

distress, including Small States, as well as IDA Gap and Blend countries (unless they are high risk Small States),

will receive a portion of their country allocations as SMLs.

• 50-year loans for IDA-only countries at moderate risk of debt distress in lieu of the previous financing terms of

half grants and half loans, with an exception for Small States. IDA-only Small States at moderate risk of debt

distress will continue to receive half grants and half loans.

See Figure 4 for Overview of IDA20 Financing Terms.

Figure 4: Overview of IDA 20 Financing Terms

12 June 30, 2022

Country Allocation Envelope represents $62.8 billion of the IDA20 resource envelope and is allocated based on the

PBA. The amount available for each country is a function of the country’s CPR rating, population, and per capita

income, complemented by the FCV envelope, where applicable. With the introduction of new financing terms in

IDA20, some IDA countries will receive a portion of their country allocations as concessional SMLs. In addition,

IDA-only countries at moderate risk of debt distress, with the exception of Small States, will receive their country

allocations as 50-year loans. Previously, these countries were eligible for half grants and half loans.

IDA Concessional Windows allow IDA to respond to specific needs of its members. In IDA20, $21.4 billion of the

IDA20 resource envelope will be used to fund the following:

• $7.9 billion of Regional Window.

• $2.4 billion of Window for Host Communities and Refugees.

• $3.3 billion of Crisis Response Window.

• $7.8 billion of Concessional Scale-up Window (SUW) – SMLs.

Regional Window

The Regional Window was developed as a funding mechanism to provide additional resources to finance projects that

help low‐income countries achieve their regional integration objectives. IDA fosters regional integration by playing

three overlapping roles:

• supporting an enabling environment through advisory and analytical work;

• financing projects through policy and investment loans; and

• convening state and nonstate actors for coordination and collective actions.

Window for Host Communities and Refugees (WHR)

The Window for Host Communities and Refugees will support operations that promote medium-to long-term

development opportunities for refugee and host communities in IDA countries. The purpose of the WHR is to support

refugee hosting countries to:

• create social and economic development opportunities for refugee and host communities;

• facilitate solutions that include sustainable socio-economic inclusion of refugees in the host country and/or their

return to the country of origin; and

• strengthen country preparedness for increased or potential new refugee flow.

Crisis Response Window (CRW)

The primary objective of the CRW is to provide IDA countries with additional resources that will help them to respond

to major natural disasters, or public health emergencies and severe economic crises, so that they can return to their

long-term development paths. The $3.3 billion window under the IDA20 resource envelope includes an allocation of

up to $1.0 billion under the CRW Early Response Financing (ERF) which will support IDA countries’ response to

slower-onset crises, namely disease outbreaks and food insecurity.

Concessional Scale-up Window – Shorter Maturity Loans (SUW-SML)

The Shorter Maturity Loans under the Scale-up Window will provide additional concessional resources with an

allocation of $7.8 billion in eligible countries i.e., IDA-only countries at low or moderate risk of debt distress, as well

as Gap and Blend countries (except Small States that are at high risk or in debt distress).

Non-Concessional Financing

Non-Concessional financing comprises loans and guarantees whose terms are aligned with those of IBRD’s flexible

loans and guarantees. Under the adjusted IDA20 resource envelope, $6.3 billion of resources have been allocated to

non-concessional financing which entirely relates to the regular Scale-up Window.

Non-Concessional Scale-up Window: The Non-Concessional Scale-up Window is a window of resources

established to enhance support for high-quality, transformational, country-specific and/or regional operations with

strong development impact. Allocation of Non-Concessional Scale-up Window resources to the regions will broadly

conform to the allocations under the PBA, excluding countries at a high risk of debt distress. Allocations are balanced

between IDA-only and Blend countries, and to avoid countries from having a concentration of Non-Concessional

Scale-up Window resources. Implementation arrangements will prioritize a country’s ability to absorb resources and

Resources

June 30, 2022 13

the proposed projects’ alignment with IDA20 policy priorities and the debt-related Sustainable Development Finance

Policy.

Private Sector Window (PSW)

The IDA-IFC-MIGA Private Sector Window was created under IDA18 to mobilize private sector investment in IDA-

only countries and IDA-eligible Fragile and Conflict-affected Situations. In IDA19, the PSW was allocated an initial

envelope of $2.5 billion which was revised to $1.7 billion under the adjusted IDA19 resource envelope. Under IDA20,

$2.5 billion has been allocated to the PSW envelope.

PSW is deployed through four facilities. These facilities have been designed to target critical challenges faced by the

private sector and will leverage IFC and MIGA’s business platforms and instruments.

During FY22, $1,107 million of the IDA19 PSW resources, net of full terminations and cancellations, were committed.

As of June 30, 2022, $879 million had been utilized out of a combined total of $2.9 billion committed in IDA18 and

IDA19. See Notes to the Financial Statements for the year ended June 30, 2022, Note G –Transactions with Affiliated

Organizations – Table G4.

Table 4: Utilization of PSW Commitments

In millions of U.S. dollars

As of June 30, 2022

IDA18

IDA19

Total

Utilization Measure

Allocation

a

$

1,282

$

1,668

$

2,950

Net Commitments

b

1,282

1,665

2,947

of which utilized

Guarantees

$

638

Face value of outstanding guarantees

Derivatives

132

Notional amount

Funding of IFC's PSW-related equity

investments

59

Amortized cost

Loans

50

Amortized cost

Total utilization of IDA PSW

$

879

a. IDA18 final allocation of $1,370 million was reduced by $88 million of cancellations which were reallocated to IDA19 PSW.

b. Of the $1,282 million net commitments under IDA18 PSW, $79 million was returned to country allocations and is no longer available

for utilization.

Arrears Clearance Framework

IDA has a policy of not providing additional financing to borrowers who are overdue on their current payments to

IDA or IBRD. However, it may engage with these countries under limited and clearly defined circumstances. IDA’s

arrears clearance framework sets out these circumstances, including (i) pre-arrears clearance grants; and (ii) the arrears

clearance set-aside, that can only be financed under the arrears clearance operations. In IDA20, no allocation was set

aside towards arrears clearance to support the possible reengagement of IDA countries that are currently in arrears.

However, during the IDA20 period, should meaningful progress arise in any country in arrears, a reallocation

discussion with IDA members will be initiated.

(i) Pre-Arrears Clearance Grants (PACG)

The PACG mechanism enables IDA to engage early in support of a government undertaking convincing reforms. This

was first introduced in IDA12 to be used to finance high priority activities related to the preparation of a program of

social and economic recovery and to build resilience until the arrears are fully cleared. Conditions constituting this

framework include indications that:

• early performance is promising as evidenced by the recipient country having taken convincing steps towards social

and economic recovery.

• arrears to IDA and/or IBRD are large and protracted and cannot be easily or quickly cleared using domestic

resources.

• a concerted international effort to provide positive financial flows and other assistance is underway, and other

creditors have agreed not to make net withdrawals of financial resources from the country.

• alternative sources of financing for post-conflict recovery are inadequate or available only on inappropriate terms;

and

14 June 30, 2022

• Pari passu sharing arrangements are in place between preferred creditors, for any payments made by the country

in advance of arrears clearance.

The PACG program has met its objectives with each of the prior PACG recipients successfully clearing all their arrears

to IDA. Prior PACG recipients are Democratic Republic of the Congo, Cote d’Ivoire, Afghanistan, Liberia, Myanmar,

Somalia, and Sudan for an amount totaling $802 million between FY01 and FY22.

(ii) Arrears Clearance Set-Aside

The arrears clearance set-aside (ACSA) forms part of IDA’s overall financing commitments. It is financed by

additional member contributions under the replenishments. In IDA15, the arrears clearance was further enhanced.

IDA members agreed to ring-fence arrears clearance support to IDA countries that were in arrears as of December 31,

2006 and meet a very narrow and well-defined set of criteria– see below, including eligibility for support under the

Heavily Indebted Poor Countries (HIPC) debt initiative. Amounts were set aside within the IDA replenishment so that

when circumstances allow, IDA would be able to help countries clear arrears and fully re-engage with the World

Bank.

To be considered for any arrears clearance support, the country would need to meet the following criteria:

• be eligible for HIPC debt relief;

• agree to implement a medium-term growth-oriented reform program endorsed by the World Bank;

• ensure a sustainable macro and sustainable debt service after arrears clearance;

• agree on a stabilization program endorsed by the International Monetary Fund (IMF) management and monitored

by IMF staff or supported by an IMF arrangement; and

• agree to a financing plan for full clearance of arrears, including normalization with other Multilateral

Development Banks (MDBs).

In addition, to receive support for arrears clearance, project proposals should meet re-engagement criteria based on

facts and circumstances of each case.

Section IV: Financial Results

June 30, 2022 15

Section IV: Financial Results

Financial Results and Portfolio Performance

Net Income

IDA had net income of $12 million in FY22 compared with a net loss of $433 million in FY21 (See Table 5). The

increase in net income during the year was primarily driven by:

• A positive change of $0.9 billion in non-functional currency translation adjustment gains/(losses) primarily

attributable to the depreciation of the majority of the non-functional currencies against the U.S. dollar in FY22

compared to the appreciation of these currencies in FY21;

• A decrease of $0.5 billion in development grant expenses primarily due to the disbursement of $1.3 billion of

development grants to Sudan in FY21 in support of the re-engagement and reform program after its arrears

clearance;

• An increase of $0.4 billion in unrealized mark-to-market gains on non-trading portfolios. The increase was mainly

driven by higher mark-to-market gains from the derivatives held for the Capital Value Protection Program (CVP),

as the increase in U.S. dollar and Euro interest rates for long tenors during the year was higher compared to FY21;

partially offset by

• A charge of $0.3 billion for provision for losses on loans and other exposures in FY22 compared to a release of

$0.5 billion in FY21 driven by a $0.8 billion release of provision after Sudan cleared its overdues in FY21.

Adjusted Net Income

Adjusted Net Income, a non-GAAP measure, reflects the economic results of IDA’s operations and is used by IDA’s

management and the Board as a financial sustainability measure. ANI is defined as IDA’s net income, adjusted to

exclude the following items.

• Development financing activities directly funded by contributions from members: These are mainly comprised of

development grants, provision for HIPC / Multilateral Debt Relief Initiative (MDRI) debt relief, amortization of

discounts on CPL. For financial reporting, these activities are treated as expenses, while contributions from

members which finance these activities, are reflected directly in IDA’s equity since they carry voting rights.

• Contributions/grants received from affiliated organizations or other similar contributions: These are mainly

comprised of contributions from IBRD, IFC and other contributions from trust funds. These are intended to finance

development activities similar to member contributions but are not directly included in equity as they do not carry

voting rights.

• Non-functional currency translation adjustment (gains) losses: These represent unrealized exchange rate

gains/losses resulting from the translation of loans, borrowings, development grants payable and all other assets

and liabilities still held on IDA’s Balance Sheet, that are denominated in currencies other than the component

currencies of SDR.

• Unrealized mark-to-market gains/losses on non-trading portfolios: These are mainly comprised of unrealized

mark-to-market gains and losses on the asset/liability management (ALM), borrowing, and non-trading investment

portfolios. For the purpose of ANI, the result of loan revenue hedges is not part of the adjustment related to

unrealized mark-to-market gains/losses on non-trading portfolio since the objective of the loan revenue hedges is

to stabilize IDA’s revenue against any currency risk.

• Unrealized mark-to-market gains/losses on certain positions in the investment trading portfolios, net: This

adjustment applies to trades where the unrealized gains and losses on derivative forward contracts are recorded in

the income statement and the underlying physical assets being purchased and sold are recorded at amortized cost

during the holding period. In these cases, the unrealized gains, and losses on the forward contract at the end of the

reporting period (if any) are excluded from net income when calculating adjusted net income. As of June 30, 2022,

there were no active trades requiring adjustment.

• Pension, Post-Employment Benefit Plan (PEBP) and Post-Retirement Contribution Reserve (PCRF) adjustments:

While IDA is not a participating sponsor to these benefit plans, IDA shares in the costs and reimburses IBRD for

its proportionate share of any contributions made to these plans by IBRD, as part of a Board-approved cost sharing

ratio. The Pension adjustment reflects the difference between IDA’s share of cash contributions to both the pension

plans and PCRF, and the accounting expense, as well as the investment revenue earned on those assets related to

Section IV: Financial Results

16 June 30, 2022

the PEBP and PCRF. The PCRF was established by the Board to stabilize contributions to the pension and post-

retirement benefits plans. Management has designated the income from these assets to meet the needs of the

pension plans. As a result, PEBP and PCRF investment revenue is excluded from adjusted net income.

• Other Adjustments:

i. Under certain arrangements (such as Externally Funded Outputs (EFOs)), IDA receives a share of the revenue

earned from agreements with donors under which funds received are to be used to finance specified outputs

or services. These funds may be utilized only for the purposes specified in the agreements and are therefore

considered contractually restricted until applied for these purposes. Income attributable to these arrangements

is excluded from reported income when determining adjusted net income since there is no discretion about the

use of these funds.

ii. Effective from FY22, the difference between fee revenue and expenses from the Reserve Advisory and

Management Partnership (RAMP) program is excluded from the reported net income to arrive at adjusted net

income. Under the Board-approved framework, RAMP fees are dedicated for the purpose of providing

technical assistance and asset management services to external clients. Due to the potential timing mismatch

between fee revenue (recognized as earned) and program expenditures (recognized as incurred), fees earned

in a given fiscal year may be used to provide services in a future fiscal year. To ensure that RAMP revenues

are only used for the delivery of RAMP services, and not allocated for other purposes, any difference between

fee revenue and expenses from RAMP included in reported net income will be excluded to arrive at adjusted

net income.

IDA’s adjusted net income was $260 million in FY22 compared with $394 million in FY21 (See Table 5). The

decrease of $134 million was primarily driven by a $90 million decrease in net interest revenue on loans mainly due

to the recognition of $244 million of service charge revenue in FY21 when Sudan paid all the overdue principal and

service charges due to IDA.

Table 5: Condensed Statement of Income

In millions of U.S. dollars

For the fiscal year ended June 30,

2022

2021

Negative

Impact

Positive

Impact

Interest revenue

Loans, net

$

1,960

$

2,050

Investments, net

189

147

Asset-liability management derivatives, net

1

(14)

Borrowing expenses, net

(249)

(187)

Interest revenue, net of borrowing expenses

$

1,901

$

1,996

Provision for losses on loans and other exposures, (charge) release

(278)

539

Other (expenses) revenue, net (Table 14)

(2)

56

Net non-interest expenses (Table 12)

(1,392)

(1,612)

Transfers from affiliated organizations and others

274

544

Non-functional currency translation adjustment gains (losses), net

511

(372)

Unrealized mark-to-market (losses) gains on investments-trading portfolio, net

a

(104)

144

Unrealized mark-to-market gains on non-trading portfolios, net

1,474

1,102

Development grants

(2,372)

(2,830)

Net Income (Loss)

$

12

$

(433)

Adjustments to reconcile net (loss) income to adjusted net income:

Expenses relating to development financing activities directly funded by

contributions from members

2,508

2,070

Contributions from affiliated organizations and others

(274)

(544)

Non-functional currency translation adjustment (gains) losses, net

(511)

372

Unrealized market-to-market gains on non-trading portfolios, net

b

(1,432)

(1,118)

Pension and other adjustments

(43)

47

Adjusted Net Income

$

260

$

394

a. Includes IDA’s share of returns from Post-Employment Benefit Plan (PEBP) and Post-Retirement Contribution Reserve

Fund (PCRF) assets – $37 million negative return (FY21- $184 million positive return).

b. Excludes $42 million of gains from revenue-related forward currency contracts (FY21 - $16 million of losses).

Section IV: Financial Results

June 30, 2022 17

Table 6: Condensed Balance Sheet

In millions of U.S. dollars

As of

June 30, 2022

June 30, 2021

Decrease

Increase

Assets

Due from banks

$

686

$

496

Investments

39,827

37,376

Net loans outstanding

a

174,490

177,779

Derivative assets, net

404

249

Other assets

4,607

3,424

Total assets

$

220,014

$

219,324

Liabilities

Borrowings

$

32,899

$

28,314

Derivative liabilities, net

579

408

Other liabilities

7,868

9,726

Equity

178,668

180,876

Total liabilities and equity

$

220,014

$

219,324

a. The fair value of IDA’s loans was $141,193 million as of June 30, 2022 ($164,606 million –June 30, 2021).

Equity

See Table 7 below for the change in IDA’s equity during FY22:

Table 7: Changes in Equity

In millions of U.S. dollars

Equity as of June 30, 2021

$

180,876

Change during the year:

Subscriptions and contributions paid-in

7,325

Nonnegotiable, noninterest-bearing demand obligations

1,265

Change in Accumulated deficit

12

Change in Accumulated other comprehensive (loss) income

(10,808)

Change in Deferred amounts to maintain value of currency holdings

(2)

Total change

(2,208)

Equity as of June 30, 2022

$

178,668

Results from Lending Activities

Loan Portfolio and Grant Activity

As of June 30, 2022, IDA’s net loans outstanding was $174.5 billion, lower by $3.3 billion compared with June 30,

2021. The decrease was mainly due to currency translation losses of $12.5 billion, consistent with the depreciation of

the SDR by 6.9% against the U.S. dollar during the year, partially offset by net disbursements of $9.1 billion during

the year.

As of June 30, 2022, 88% of IDA’s total loans outstanding were denominated in the SDR. For the regional presentation

of total loans outstanding, see Notes to the Financial Statements for the year ended June 30, 2022, Note D – Loans

and Other Exposures – Table D8.

Provision for losses on loans and other exposures

In FY22, IDA recorded a provision for losses on loans and other exposures of $278 million primarily due to the

increase in exposure during the year. This compares to a $539 million release of provision in FY21 mainly due to an

$831 million release of loan loss provision after Sudan cleared its arrears in March 2021 (see Notes to the Financial

Statements for the year ended June 30, 2022, Note D – Loans and Other Exposures – Table D5).

For adjusted net income purposes, the provision for losses on loans and other exposures excludes the provision for

debt relief under HIPC/MDRI and the provision for grant advances since these are funded by contributions from

members.

690

(2,208)

(1,858)

171

4,585

690

1,183

155

(3,289)

2,451

190

Section IV: Financial Results

18 June 30, 2022

Table 8: Provision for losses on loans and other exposures

In millions of U.S. dollars

For the fiscal year ended June 30,

2022

2021

Variance

Provision for losses on loans and other exposures, (charge) release

Loans and other exposures

$

(283)

$

(289)

$

6

Debt relief under HIPC/MDRI

5

828

(823)

Total

$

(278)

$

539

$

(817)

Table 9: Net Loans Outstanding Activity

In millions of U.S. dollars

Net Loans outstanding as of June 30, 2021

$

177,779

Change during the year:

Gross loan disbursements

15,860

Loan repayments

(6,738)

Change in accumulated provision for loan losses

a

135

Translation adjustments

(12,505)

Other

b

(41)

Total change

(3,289)

Net Loans outstanding as of June 30, 2022

$

174,490

a. Includes translation adjustments on accumulated provision for loan

losses and debt relief under HIPC/MDRI. See Notes to the Financial

Statements, Note D – Loans and other exposures.

b. Includes deferred loan origination costs of $11 million, and HIPC debt

relief provided of $30 million.

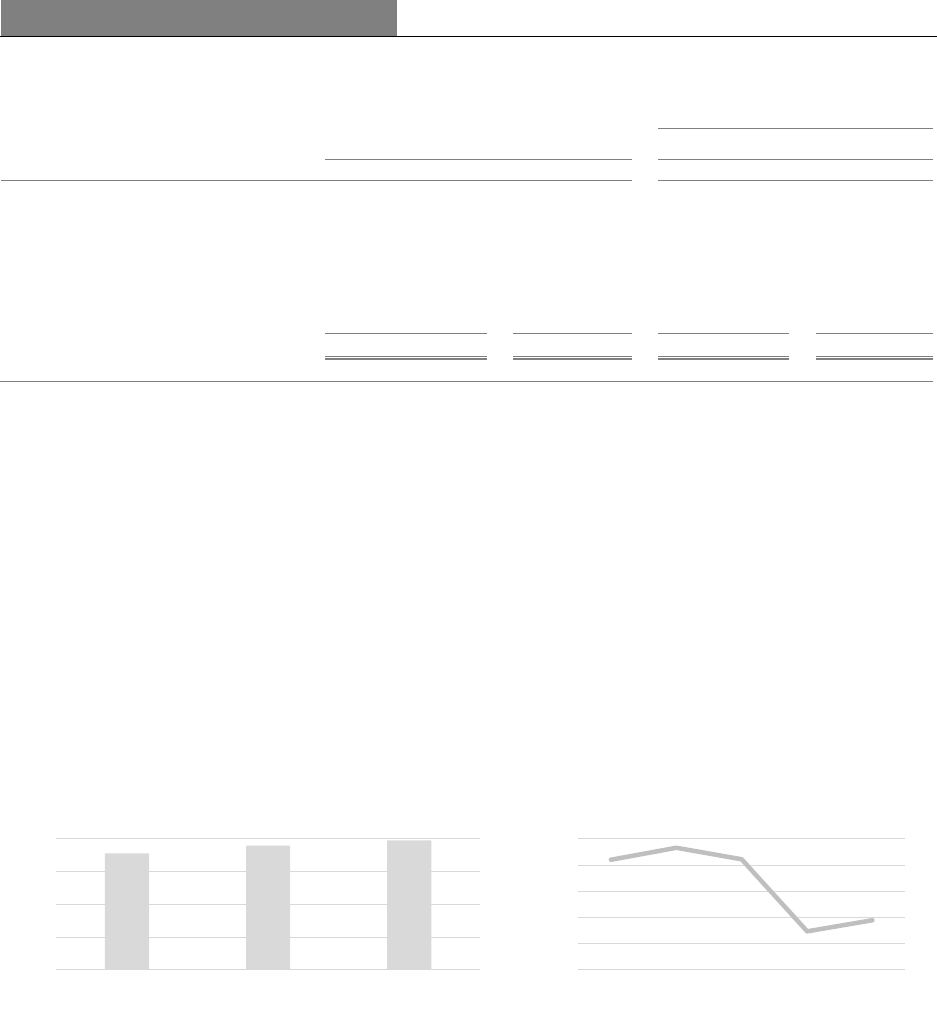

Figure 5: Net Loans Outstanding

In billions of U.S. dollars

IDA’s loans generally disburse within five to ten years for Investment Project Financing (IPF), and one to three years

for Development Policy Financing (DPF). Therefore, each year’s disbursements also include amounts relating to

commitments made in earlier years (See Table 10).

Table 10: Gross Disbursements of Loans and Grants by Region

In millions of U.S. dollars

2022

2021

For the fiscal year ended June 30,

Loans

a

Grants

b

Total

Loans

a

Grants

b

Total

Variance

Eastern and Southern Africa

$

4,520

$

2,613

$

7,133

$

4,785

$

3,296

$

8,081

$

(948)

Western and Central Africa

4,942

1,602

6,544

4,384

1,661

6,045

499

East Asia and Pacific

1,365

137

1,502

1,186

111

1,297

205

Europe and Central Asia

631

133

764

736

144

880

(116)

Latin America and the Caribbean

346

164

510

369

126

495

15

Middle East and North Africa

63

496

559

70

309

379

180

South Asia

3,952

250

4,202

5,145

599

5,744

(1,542)

Total

$

15,819

$

5,395

$

21,214

$

16,675

$

6,246

$

22,921

$

(1,707)

a. Excludes PSW related disbursements - $41 million (FY21 - $6 million).

b. Excludes Project Preparation Advances (PPA).

As of June 30, 2022, 59% of IDA’s loans were on regular terms (75 basis points SDR equivalent service charge) see

Table 11. The decrease in IDA’s revenue from loans in FY22 compared to FY21 was primarily due to $244 million

of service charges recorded in March 2021 when Sudan paid all its overdue principal and charges due to IDA.

161

178

174

0

50

100

150

200

Jun 20 Jun 21 Jun 22

Section IV: Financial Results

June 30, 2022 19

Table 11: Revenue and Balances by Product Category

In millions of U.S. dollars

Interest revenue on loans

a

Balance as of June 30,

For the fiscal year ended June 30,

Category

2022

2021

2022

2021

Loans

Concessional

Regular

$

104,716

$

109,612

$

829

$

1,055

Blend

65,617

65,203

970

862

Hard

b

1,327

1,406

47

49

Non-concessional

c

6,381

5,273

116

85

Others

d

50

10

1

1

Total

$

178,091

$

181,504

$

1,963

$

2,052

a. Excludes interest rate swap expenses related to loan hedges - $3 million ($2 million in FY21).

b. Prior to July 1, 2017, IDA offered Hard-Term loans to Blend Countries (excluding Small Island Economies). Hard-term loans are no

longer offered.

c. In addition, $24 million of commitment charges were earned in FY22 on undisbursed balances of non-concessional loans ($19

million in FY21).

d. Represents loans under the PSW.

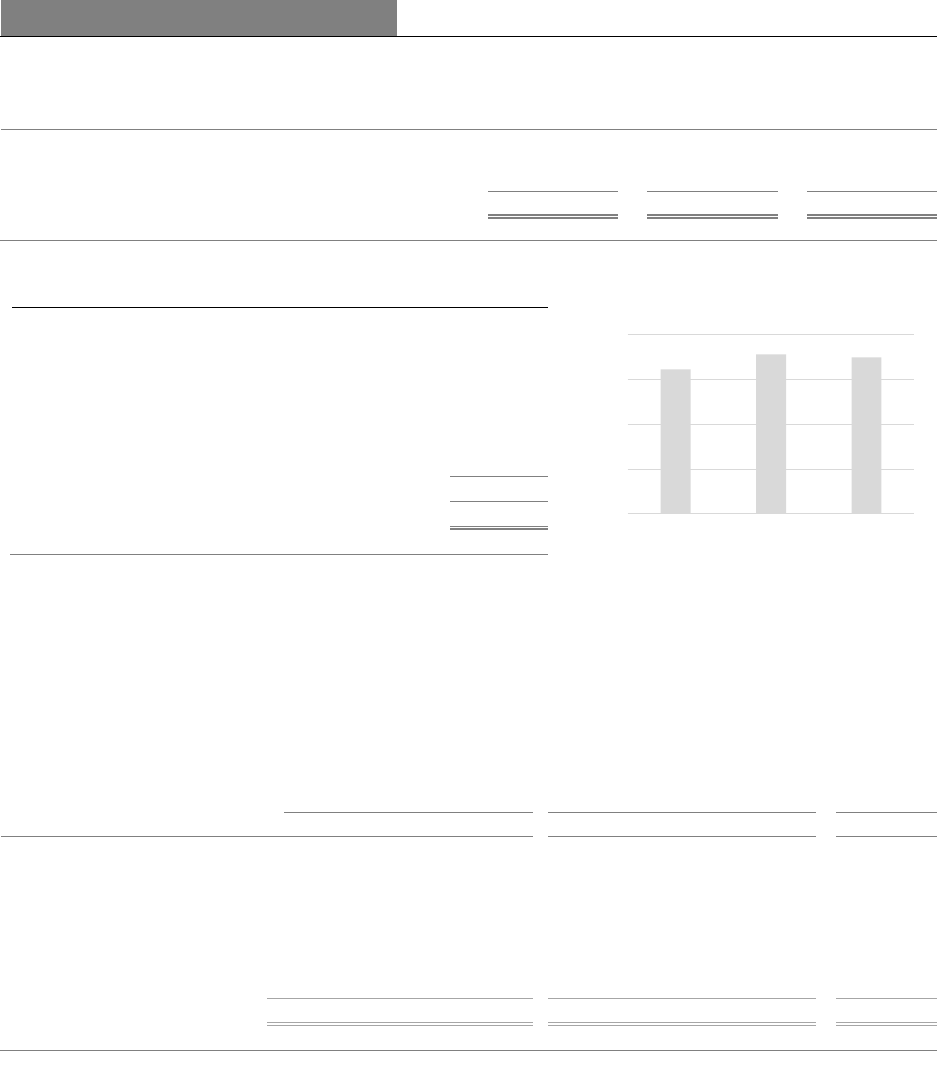

Results from Investing Activities

Investment Portfolio

IDA’s net investment portfolio increased to $39.6 billion as of June 30, 2022, from $37.9 billion as of June 30, 2021.

The increase was primarily due to the investment of cash received from member contributions and proceeds from net

new debt issuances, partially offset by net loan and grant disbursements.

Investment interest revenue, net of derivatives

During FY22, IDA’s net interest revenue from investments was $189 million, an increase of $42 million compared

with FY21. The increase in interest revenue was mainly driven by the higher average interest rate environment in the

current year and the higher average balance of the portfolio.

Figure 6: Net Investment Portfolio

In billions of U.S. dollars

Figure 7: Net Investment Revenue

In millions of U.S. dollars

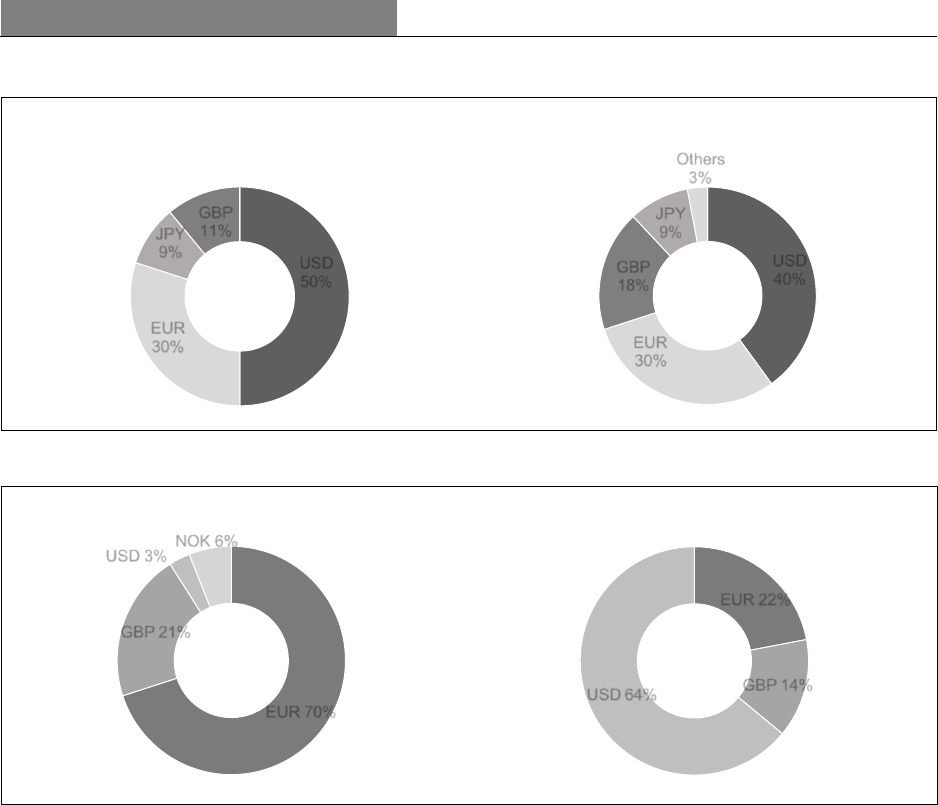

Results from Borrowing Activities (excluding associated derivatives)

As of June 30,2022, Market borrowings recorded at fair value were $19.7 billion, a decrease of $0.9 billion compared

to June 30, 2021 ($20.6 billion). The decrease was driven mainly by the impact of increasing interest rates and

translation gains during the year. See Notes to the Financial Statements for the year ended June 30, 2022, Note E –

Borrowings.

As of June 30, 2022, the market borrowings at amortized cost were $6.2 billion (Nil – June 30, 2021). In FY22, IDA

started to issue long-term fixed rate market debt to fund fixed rate loans and the new issuances during the year were

$6.2 billion. See Notes to the Financial Statements for the year ended June 30, 2022, Note E – Borrowings.

Concessional partner loans from members, recorded at amortized cost were $7.0 billion ($7.7 billion - June 30, 2021).

The decrease of $0.7 billion was mainly due to translation adjustment gains.

35.6

37.9 39.6

0

10

20

30

40

Jun 20 Jun 21 Jun 22

0

100

200

300

400

500

FY18 FY19 FY20 FY21 FY22

Section IV: Financial Results

20 June 30, 2022

Figure 8: Borrowings

In billions of U. S. dollars

Transfers from Affiliated Organizations

Since 1964, IBRD has made transfers to IDA out of its net income, upon approval by the Board of Governors. Under

a formula-based approach for IBRD's income support to IDA, the amount of income transfer recommended for IDA

is a function of IBRD's financial results. On October 14, 2021, IBRD’s Board of Governors approved a transfer from

FY21 allocable income of $274 million to IDA which was received by IDA on October 25, 2021.

Net Non-Interest Expense

As shown in Table 12, IDA’s net non-interest expenses are primarily comprised of administrative expenses, net of

revenue from externally-funded activities. IBRD and IDA's administrative budget is a single resource envelope that

funds the combined work programs of IBRD and IDA. The allocation of administrative expenses between IBRD and

IDA is based on an agreed cost and revenue sharing methodology, approved by their Boards. The allocation is

primarily driven by the relative level of activities relating to lending, knowledge services and other services between

the two institutions. The administrative expenses shown in the table below include costs related to IDA-executed trust

funds and other externally funded activities.

IDA’s net non-interest expenses on a GAAP basis were $1,392 million in FY22, compared to $1,612 million in FY21.

The key driver for the decrease was the decrease in pension costs, primarily driven by the higher asset returns in FY21,

which resulted in lower amortization of unrecognized actuarial losses in FY22.

IDA’s net non-interest expenses for adjusted net income purposes were $1,472 million in FY22, compared to $1,381

million in FY21, an increase of $91 million. FY21’s net non-interest expenses were significantly impacted by COVID-

19-related restrictions. FY22’s increase was driven by higher travel expenses due to the gradual easing of COVID-19-

related travel restrictions/office closures, inflationary cost pressures, the acceleration of work programs from the high

level of lending activities during the year as well as additional support and engagement in FCV countries to address

the growing needs and the increase in conflict situations. As a result, travel costs increased by $56 million but are still

less than what they were before the COVID-19 pandemic, approximately 38% of FY19 costs. The cost of operating

in FCV countries also affected expenses including costs associated with evacuations and security in dangerous

situations.

12.1

20.6

19.7

6.2

7.6

7.7

7.0

0

10

20

30

40

Jun 20 Jun 21 Jun 22

Concessional partner loans, at amortized cost

Market borrowings, at amortized cost

Market borrowings, at fair value

Section IV: Financial Results

June 30, 2022 21

Table 12: Net Non-Interest Expenses

In millions of U.S. dollars

For the fiscal year ended June 30,

2022

2021

Variance

Administrative expenses:

Staff costs

$

1,137

$

1,121

$

16

Travel

71

15

56

Consultant and contractual services

588

544

44

Pension and other post-retirement benefits

191

494

(303)

Communications and technology

83

68

15

Premises and equipment

144

135

9

Other expenses

24

29

(5)

Total administrative expenses

a

$

2,238

$

2,406

$

(168)

Contributions to special programs

b

19

20

(1)

Revenue from externally funded activities:

Reimbursable advisory services

(41)

(46)

5

Reimbursable revenue - IDA-executed trust funds

(613)

(553)

(60)

Revenue trust funds administration

(43)

(38)

(5)

Restricted revenue

(3)

(15)

12

Other revenue

(165)

(162)

(3)

Total revenue from externally funded activities

$

(865)

$

(814)

$

(51)

Total Net Non-Interest Expenses (Table 5) - GAAP Basis

$

1,392

$

1,612

$

(220)

Adjustments to arrive at Net non-interest expenses - Adjusted Net

Income basis

Pension, RAMP and EFO adjustments (Table 13)

c

80

(231)

311

Net non-interest expenses - Adjusted Net Income basis

$

1,472

$

1,381

$

91

a. Includes expenses related to IDA executed trust funds of $613 million for FY22 and $553 million for FY21.

b. Included in Non-interest expenses – Other in the Statement of Income.

c. Adjustments are included in the Pension and other adjustments line in Table 5. The RAMP adjustment was effective in FY22 and

made prospectively.

IDA’s goal is to have its net administrative expenses covered by its loan revenue (interest, service charges,

commitment fees, and guarantee fees). Thus, IDA monitors its net administrative expenses as a percentage of its loan

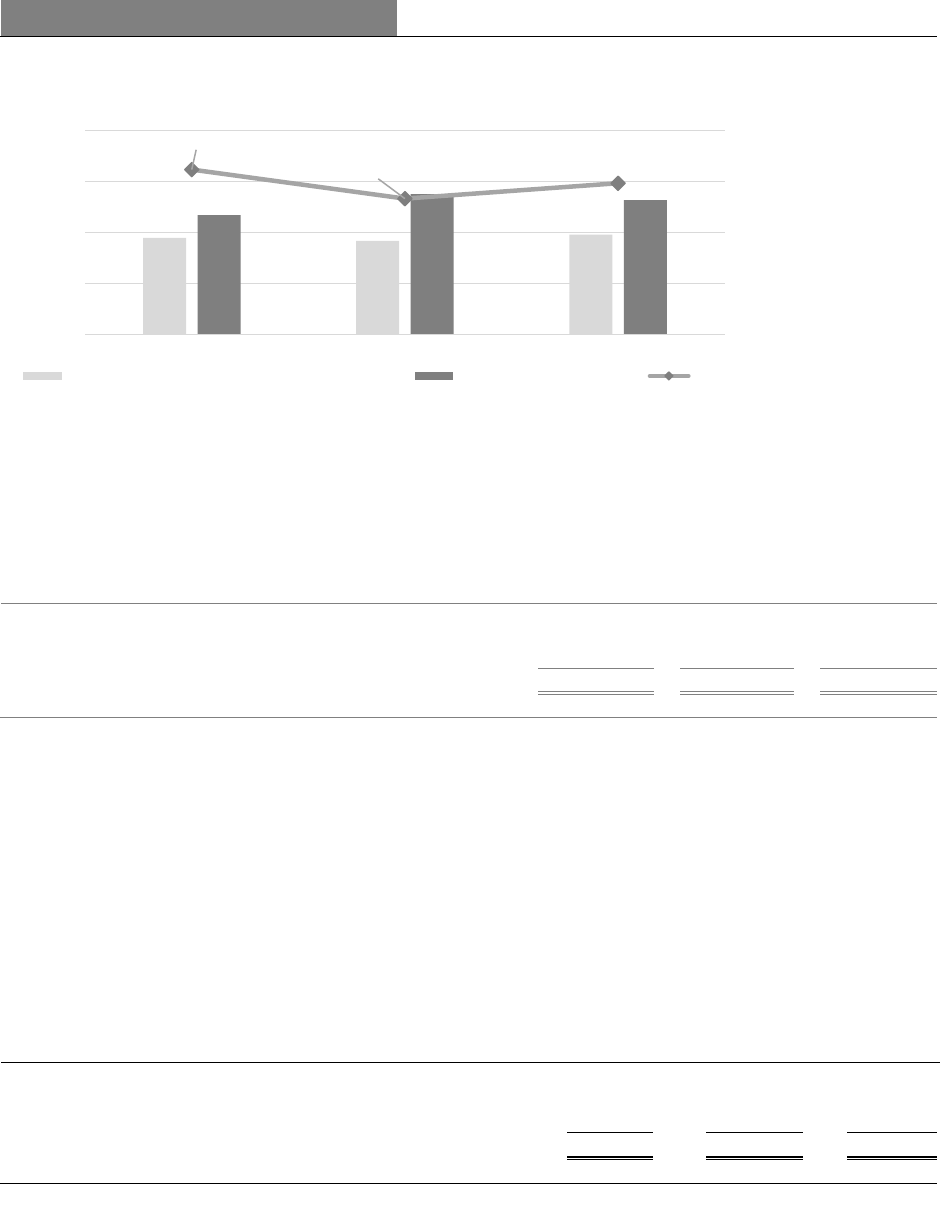

revenue, using a measure referred to as the budget anchor. In FY22, IDA’s budget anchor was 74.3%, higher by 7.6

percentage points compared to FY21 primarily due to the one-time effect of $244 million of service charges recognized

in FY21 when Sudan paid all its overdue principal and charges due to IDA. Excluding the impact of Sudan’s arrears

clearance of $244 million in FY21, IDA’s FY22 budget anchor improved by 1.3%. See Table 13.

Table 13: Budget Anchor

In millions of U.S. dollars

For the fiscal year ended June 30,

2022

2021

Variance

Total net Non-interest Expenses (Table 12)

$

1,392

$

1,612

$

(220)

Pension, RAMP and EFO adjustments (Table 12)

a

80

(231)

311

Net administrative expenses for Budget Anchor

$

1,472

$

1,381

$

91

Interest Revenue from Loans, net of associated borrowing expenses

$

1,892

$

2,050

$

(158)

Commitment fee and Guarantee fee revenue (Table 14)

46

36

10

Gains (losses) on revenue-hedging forward currency contracts

42

(16)

58

Total revenue for Budget Anchor

$

1,980

$

2,070

$

(90)

Budget Anchor

74.3%

66.7%

7.6%

a. These adjustments are made to arrive at net administrative expenses used for adjusted net income purposes.

Section IV: Financial Results

22 June 30, 2022

Figure 9: Budget Anchor

In millions of U.S. dollars, except ratio in percentages

In FY22, IDA’s net other expenses were $2 million as the PPA grant expenses exceeded PPA cancellations and

refinancing of PPA grants previously approved. In contrast, in FY21, IDA had $56 million of net other revenue as

PPA cancellations and refinancing of PPA grants previously approved exceeded PPA grant expenses. Refinanced PPA

grants are included in the loan provided to the borrower, and correspondingly, prior grant expenses are reversed.

Table 14: Other (Expenses) Revenue, net

In millions of U.S. dollars

For the fiscal year ended June 30,

2022

2021

Variance

PPA grants and others

$

(48)

$

20

$

(68)

Guarantee fees

22

17

5

Commitment charges

24

19

5

Other (Expenses) Revenue, net (Table 5)

$

(2)

$

56

$

(58)

Unrealized mark-to-market gains (losses) on investments- trading portfolio

IDA’s investments-trading portfolio, excluding the returns from the PEBP, had unrealized mark-to-market losses of

$67 million in FY22, compared to unrealized mark-to-market losses of $40 million in FY21. The losses in both years

were mainly due to the increase in yields on long-term euro government bonds.

Unrealized mark-to-market gains (losses) on non-trading portfolios, net

During FY22, the non-trading portfolios had $1.5 billion of net unrealized mark-to-market gains ($1.1 billion net

unrealized mark-to-market gains in FY21). The increase is mainly driven by unrealized mark-to-market gains from

the derivatives held for the CVP, managed as part of ALM, as the U.S. dollar and EUR interest rates for long tenors

increased more in FY22 compared to FY21. (Section IX: Risk Management).

Table 15: Unrealized Mark-to-Market gains (losses) on non-trading portfolios, net

In millions of U.S. dollars

For the fiscal year ended June 30

2022

2021

Variance

Asset-liability management derivatives

$

1,441

$

1,080

$

361

Investment portfolio

(26)

(12)

(14)

Other

a

59

34

25

Total

$

1,474

$

1,102

$

372

a. Other comprises mark-to-market gains (losses) on the borrowings, loan related derivatives and on PSW.

81.0%

66.7%

74.3%

0%

20%

40%

60%

80%

100%

0

750

1,500

2,250

3,000

FY20 FY21 FY22

Net administrative expenses for budget anchor Budget Anchor Revenue Budget Anchor

Section IV: Financial Results

June 30, 2022 23

Non-functional currency translation adjustment gains (losses), net

Non-functional currency translation adjustment gains or losses represent unrealized exchange rate gains or losses

resulting from the hedging of exchange rate risk related to future donor contributions, and the translation of loans,

borrowings, and all other assets and liabilities held on IDA’s Balance Sheet, that are denominated in currencies other

than the SDR and its component currencies. The translation adjustment gains and losses in FY22 and FY21 were

primarily driven by the hedging of exchange rate risk related to future donor contributions. Certain members pledge

their future equity contributions in non-SDR currencies. These future cash flows are economically hedged using

currency forwards. The economic offset is inherent in the future contribution inflows. The payable portion of the

currency forward contracts are denominated in non-functional currencies. The appreciation or depreciation of these

currencies against the U.S. dollar results in exchange rate gains or losses which are recorded in the income statement.

Accordingly, the translation adjustment gains of $511 million in FY22 were driven by the depreciation of the hedged

non-functional currencies against the U.S. dollar, while the translation adjustment losses of $372 million in FY21

were due to the appreciation of these currencies against the U.S dollar.

Section V: Development Activities, Products and Programs

24 June 30, 2022

Section V: Development Activities, Products and Programs

Lending Framework

IDA provides financing to lower-income countries primarily through loans, grants and guarantees. IDA has a common

framework which extends across all its development activities. The main elements of this framework are financing

principles, financing cycles and financing categories.

Financing Principles

IDA’s operations are required to conform to the general principles derived from its Articles of Agreement. These

principles are described in Box 2. Within the scope permitted by the Articles of Agreement, application of these

financing principles must be developed and adjusted in light of experience and changing conditions.

Financing Cycles

The process of identifying and appraising a project and approving and disbursing the funds often extends over several

years. However, in response to emergency situations, such as natural disasters and financial crises, IDA is able to

accelerate the preparation and approval cycle. In most cases, IDA’s Board approves each loan, grant, and guarantee

after appraisal of a project by staff. Under a Multiphase Programmatic Approach (MPA) approved by the Board in

FY18, the Board may approve an overall program framework, its financing envelope and the first appraised phase,

and then authorize management to appraise and commit financing for later program phases. Disbursements are subject

to the fulfillment of conditions set out in the loan or grant agreement. IDA used this approach to expedite support for

COVID-19 related projects. As of June 30, 2022, $12.0 billion was committed under the MPA, of which $6.7 billion

was COVID-19 related commitments.

During implementation of IDA-supported operations, staff review progress, monitor compliance with IDA’s policies,

and assist in resolving any problems that may arise. An independent unit, the Independent Evaluations Group, also

assesses the extent to which operations have met their major objectives, and these evaluations are reported directly to

the Board.

Financing Categories

Most of IDA’s lending is of three types: investment project financing, development policy financing, and program-

for-results. Figure 10 shows the percentage of loans approved for investment lending, development policy operations

and program-for-results over the past five years.

Box 2: Financing Principles

(i) IDA may provide financing for its development operations in the form of loans, grants, and guarantees directly to its members,

public or private entities and regional or public international organizations.

(ii) productivity, and thus

for technical, economic, financial, institutional, and environmental soundness. Specific provisions apply to development policy

financing, including the treatment of the macroeconomic framework, poverty and social impact, environment, forests, and other

natural resources.

(iii)

including assessments of its resources and ability to generate sufficient foreign currencies to meet debt-service obligations.

(iv)

requirements), the recipient would be unable to obtain financing under conditions which, in the opinion of IDA, are reasonable

for the recipient. This would include loans made by private sources or IBRD.

(v) The use of funds by recipients is supervised. IDA makes arrangements intended to ensure that funds provided are used only

for authorized purposes and, where relevant, with due attention to considerations of cost-effectiveness. This policy is enforced

nced

with the proceeds of loans or grants are made in conformity with the applicable financing agreements, and (b) to maximize

competition in the procurement of goods and services by using, wherever possible, international competitive bidding

procedures or, when it is not appropriate, other procedures that ensure maximum economy and efficiency. In addition, IDA

considers the use of recipient country procurement, financial management and environmental and social safeguard systems

in selected operations once these systems and capacity have been assessed by IDA as acceptable.

Section V: Development Activities, Products and Programs

June 30, 2022 25

Figure 10: Net Annual Commitments and share of financing categories

In billions of U.S. dollars, except rates in percentages

Investment Project Financing (IPF)

IPF provides financing for a wide range of activities aimed at creating the physical and social infrastructure necessary

to reduce poverty and create sustainable development. IPF is usually disbursed over the long-term (roughly a 5 to 10-

year horizon).

FY22 net commitments under IPF totaled $29.9 billion, compared with $24.7 billion in FY21.

Development Policy Financing (DPF)

DPF aims to support the borrower in achieving sustainable development through a program of policy and institutional

actions. Examples of DPF projects include strengthening public financial management, improving the investment

climate, addressing bottlenecks to improve service delivery, and diversifying the economy. DPF supports such reforms

through non-earmarked general budget financing. DPF provides fast-disbursing financing (roughly 1 to 3 years) to

help borrowers address actual or anticipated financing requirements.

FY22 net commitments under DPF totaled $3.4 billion, compared with $7.0 billion in FY21.

Program-for-Results (PforR)