Markel Segment Specialization Program

Rehabilitation

Tax Credit

n....,...

__

.,:

lIIIIflII!IilfllSpi!' s ,

..

""

t f"

n.,

__

ul.lll_al

.....

.....,~Ildw

·

il~

Di1i

"J

tl_.~

io

..

~s-.

.~iII

l.t*'S-Gc

r OIb9J"

'lliI'-"'_~,

Ihoo.1ld

or

...

nriIg,...-..tr.

~

..

ciI>

__

..

_te_OIc!101.

"

adaiIfb..q

II'

'

...........

pc:an..

fJjIRS

Dl4:w~

..

lcl

III

T-.y

INImII

AI.

...

SIntce

TIlIirq 3141(1 (R..CI:!r.m!)

CI&*Ig

IU!aIr

431'1111

-:

"'lp

'The

I{5

cfi!lission

Provide

America's

taxpayers

top

quality

service

by

helping

them

understand

and

meet

their

tax

responsibilities

and

by

applying

the

tax

law

with

integrity

and

fairness

to

all.

flJIRS

D

........

_

Rehabilitation Tax Credit

TABLE OF CONTENTS

Page No.

CHAPTER 1 --INTRODUCTION

General Background Regarding Credit 1-1

Legislative History 1-1

Passive Activity Rules 1-3

CHAPTER 2 -- CERTIFICATION PROCESS 2-1

CHAPTER 3 -- CERTIFICATION REQUIREMENTS

Background 3-1

Late Submission of Historic Preservation Certification Application 3-3

Late Submissionf of Part 1 3-3

Late Submission of Part 3 3-4

Statute of Limitations 3-5

Audit Techniques 3-5

Certification Law Sections 3-5

Court Cases 3-6

CHAPTER 4 -- NON-HISTORIC CREDITS

Background 4-1

Decertification Procedures 4-2

Non-Historic Credits Law 4-3

Court Cases 4-3

CHAPTER 5 -- PLACED IN SERVICE

Background 5-1

Acquiring Property Rules 5-2

Tax Credit Recapture 5-2

Audit Techniques 5-2

Placed in Service Law 5-3

Court Case 5-3

v 3149-109

CHAPTER 6 -- SUBSTANTIAL REHABILITATION

Background 6-1

The Substantial Rehabilitation Test 6-1

The 60-Month Alternative Test Period 6-3

Multiple Overlapping Test Periods 6-4

Multiple Building Complex for Purposes of the Substantial Rehabilitation Test 6-4

Audit Considerations 6-5

Substantial Rehabilitation Test Tax Law 6-5

Court Case 6-7

CHAPTER 7 -- BASIS REDUCTION REQUIRED

Background 7-1

Basic Reduction Law 7-2

CHAPTER 8 -- STRAIGHT LINE COST RECOVERY

Background 8-1

Straight Line Depreciation Required 8-1

Law 8-1

Court Cases 8-1

CHAPTER 9 -- CREDIT RECAPTURE ON DISPOSITION

Background 9-1

Disposition of Partnership Interest 9-1

When a Building Is Removal from National Register 9-1

Recapture When Property Is Destroyed by Casualty 9-2

When Recapture Is Not Required 9-2

Basis Adjustment Upon Recapture 9-3

Audit Techniques 9-3

Credit Recapture Law 9-4

Court Case 9-4

CHAPTER 10 -- NO CREDIT FOR ACQUISITION COSTS

Background 10-1

Audit Technique 10-1

Acquisition Cost Law 10-2

3149-109 vi

CHAPTER 11 -- ENLARGEMENT COSTS EXCLUDED

Background 11-1

Issues 11-1

Audit Technique 11-1

Enlargement Expenditures Law 11-2

CHAPTER 12 -- SITEWORK EXPENDITURES EXCLUDED

Background 12-1

Recommended Audit Techniques/Procedures 12-1

Sitework Expenditures Law 12-2

CHAPTER 13 -- PERSONAL PROPERTY EXCLUDED

Background 13-1

Personal Property Law 13-1

Court Cases, Revenue Rulings, and Senate Finance Committee Report 13-2

Court Cases 13-2

Revenue Rulings 13-3

Senate Finance Committee Report 13-3

CHAPTER 14 -- TAX EXEMPT USE PROPERTY

Background 14-1

Disqualified Lease Rules 14-1

The 35 Percent Threshold Test 14-2

Property Owned by Partnerships with Taxable and Tax-Exempt Partners 14-3

Disqualified Lease Rule Examples 14-3

Audit Techniques 14-4

Tax Law 14-4

Acknowledgement 14-5

CHAPTER 15 -- EXPENDITURES OF LESSEE

Background 15-1

Substantial Rehabilitation Test 15-1

Pass-Through Election by Lessor 15-2

Basis and Income Implications 15-3

Short-Term Lease Election 15-3

Net Lease 15-4

Audit Techniques 15-4

Court Case 15-4

vii 3149-109

CHAPTER 16 -- CONSTRUCTION INTEREST AND TAXES

Background 16-1

Audit Techniques 16-1

Construction Interest and Taxes Law 16-2

CHAPTER 17 -- PROGRESS EXPENDITURES

Background 17-1

Progress Expenditure Law 17-2

CHAPTER 18 -- FACADE EASEMENT

Background 18-1

Audit Techniques 18-3

Facade Easement Court Cases/Revenue Rulings 18-3

CHAPTER 19 -- DEVELOPER FEES

Background 19-1

Types of Developer Fees 19-1

Non-Qualifying Costs 19-3

Timing of Expense 19-5

Court Case 19-5

Position Paper 19-6

CHAPTER 20 – TAX EFFECT OF GRANT MONEY

Background 20-1

Grants Received by Non-Corporate Taxpayers 20-1

Grants Received by Corporate Taxpayers 20-2

Non-Taxable Grants 20-2

Effect of Grant Proceeds on Basis 20-3

Substantial Rehabilitation Test 20-3

Conclusion 20-4

Audit Techniques 20-4

Resources 20-4

CHAPTER 21 – SPECIAL ALLOCATION OF CREDIT

Overview 21-1

Tax Credits in General 21-1

Allocation of the Rehabilitation Tax Credit 21-3

3149-109 viii

CHAPTER 22 -- PASSIVE ACTIVITY RESTRICTIONS

Background 22-1

Passive Activity Restrictions - Taxpayer with AGI over $250,000 22-1

Passive Activity Restrictions - Taxpayer with AGI underr $250,000 22-2

Net Passive Income 22-2

Circumstances When Rehabilitation Tax Credit Is Not Limited 22-3

Audit Techniques 22-4

Court Case 22-4

Passive Activity Tax Code Provisions 22-5

CHAPTER 23 -- SYNOPSIS OF LOW INCOME HOUSING CREDIT PROVISIONS

Background 23-1

Provisions Regarding Low Income Housing 23-1

Income Targeting 23-2

Allowable Credit Percentages 23-2

When the Credit May Be Claimed 23-3

Effects of Federal Grants 23-3

Effects of Loans/Federal Subsidy 23-3

Recapture Provisions 23-4

State Housing Credit Ceiling 23-4

Low Income Housing Credit Claimed in Conjunction with

the Rehabilitation Tax Credit 23-5

CHAPTER 24 – MODIFICATIONS TO MEET THE AMERCIANS

WITH DISABLITY ACT

Background 24-1

Disabled Access Credit 24-1

Making Historic Properties Accessable 24-2

Tax Law Application 24-2

CHAPTER 25 – CONSIDERATION OF PENALTIES

Background 25-1

ix 3149-109

Chapter 1

INTRODUCTION

GENERAL BACKGROUND

Prior to 1976, there existed no tax incentive to rehabilitate or preserve historic

buildings. The Tax Reform Act of 1976 added IRC section 191 which permitted

taxpayers to amortize over a 60-month period certain expenditures to rehabilitate

property listed in the National Register of Historic Places or property located in

Registered Historic Districts and certified as significant to the district.

The 60-month amortization period was enhanced to a 10 percent rehabilitation tax

credit in 1978. In 1981, Congress expanded the rehabilitation tax credit to a three-tier

credit; a 25 percent credit for "historic rehabilitations," a non-historic rehabilitation

credit of 20 percent for buildings at least 40 years old, and a 15 percent credit for

buildings at least 30 years old.

The rehabilitation tax credit survived the Tax Reform Act of 1986, but imposed

several constraints that made the rehabilitation tax credit less attractive to individual

real estate investors. The credit was retained as a two-tier credit with a 20 percent

credit available for historical buildings and a 10 percent credit for non-historic

buildings which were first placed in service before 1936.

The Historic Preservation Tax Incentives Program, jointly administered by the

National Park Service and the State Historic Preservation Offices, is the nation’s most

effective Federal program to promote urban and rural revitalization and to encourage

private investment in rehabilitating historic buildings. The tax credit applies

specifically to preserving income-producing historic property and has generated

billions of dollars in historic preservation activity since its inception in 1976. Its

tremendous effects are evident in not only the major cities in the United States, but

also in many small towns and communities throughout the country. The completed

projects have brought renewed life to deteriorated business and residential districts,

created new jobs and new housing units, increased local and state revenues, and

helped ensure the long-term preservation of irreplaceable cultural resources.

LEGISLATIVE HISTORY

Before 1976, there were no incentives for restoring or rehabilitating older buildings in

our Nation's tax laws. Prior law actually encouraged the destruction of these

buildings by allowing deductions related to their demolition. In addition, the erection

of newer buildings in their place benefited from quicker depreciation methods.

1-1 3149-109

The year 1976 was the first year that Congress endeavored to shape public policy

regarding the preservation and rehabilitation of older buildings through our Nation's

tax laws. The Tax Reform Act of 1976 made four major law changes regarding the

treatment of deductions in reference to older buildings. These law changes became a

foundation for the current tax provisions regarding rehabilitation.

1. A provision to allow a 5-year amortization of rehabilitation expenditures. (Costs

except land and original shell.)

2. Alternative to the above which allowed for accelerated method of depreciation to

be used on both the shell and rehabilitation costs.

3. A provision which allowed only a straight-line method of depreciation on any

new building constructed where an older building had been demolished.

4. A prohibition against any deduction or recognition for tax purposes of any costs

for demolition or site clearing and no deduction for the purchase price of the

property, (building before demolition).

The next tax change, the Revenue Act of 1978, brought about an additional incentive

in the form of a tax credit. This tax credit, at a rate of 10 percent, was available in

place of the 5-year amortization from the 1976 Tax Reform Act. Congress believed

that a credit at a rate of 10 percent, similar to the Investment Tax Credit, would be

more attractive to owners or investors than amortization or depreciation deductions.

In 1981, the Economic Reform Tax Act brought about the most substantial tax credit

incentives for rehabilitation to date. In addition to historical buildings, the new law

also recognized older non-historical buildings, and allowed credits to rehabilitate

buildings at least 30 years old. The credits for rehabilitation were in a three tier

system as outlined below:

1. Buildings at least 30 years old were allowed a 15 percent credit for qualifying

rehabilitation expenditures.

2. Buildings at least 40 years old were allowed a 20 percent credit for qualifying

rehabilitation expenditures.

3. Qualifying rehabilitation expenditures for a "Certified Historic Rehabilitation"

were allowed a 25 percent credit.

The next change affecting the rehabilitation provisions came as part of the Tax

Reform Act of 1986. This Tax Reform Act was one of the most comprehensive and

sweeping changes in our Nation's history. Although many deductions and most

credits were eliminated, the Rehabilitation Credit provisions were retained with only

minor modifications. The credit is now a two-tier credit as outlined below:

3149-109 1-2

1. A 10 percent credit available for the rehabilitation of non-historic buildings with

an additional requirement that the building must have been originally constructed

before 1936, or

2. A 20 percent credit available for the rehabilitation of a Certified Historic

Structure, (one listed on the National Register of Historic Places or located in a

Registered Historic District and determined to be of significance to the Historical

District).

The actual law provisions surrounding this two-tier credit, as enacted by the Tax

Reform Act of 1986, are very similar to those under prior law. Many of the principles

regarding the application of the law and Congressional intent date back to the original

law to preserve historical buildings as enacted in 1976.

The most recent change affecting the rehabilitation tax credit was a provision of the

Revenue Reconciliation Act of 1990. This change only slightly altered the content of

prior provisions by moving the location of the provisions from IRC section 48(g) to

IRC section 47.

PASSIVE ACTIVITY RULES

The Tax Reform Act of 1986 introduced "passive activity loss provisions" that were

intended to stop "abusive tax shelters" that had plagued our tax system. Although not

directly related, these changes materially impacted the availability of the

rehabilitation tax credit to certain investors. Because of these changes, some

investors are restricted to amount of credit they may claim. Those investors with

adjusted gross income over $250,000 may be totally precluded from taking any credit.

The effect of these passive activity restrictions has significantly changed the type of

individual investor who can benefit from rehabilitation tax credit projects as well as

the entity form of ownership.

1-3 3149-109

This page intentionally left blank.

3149-109 1-4

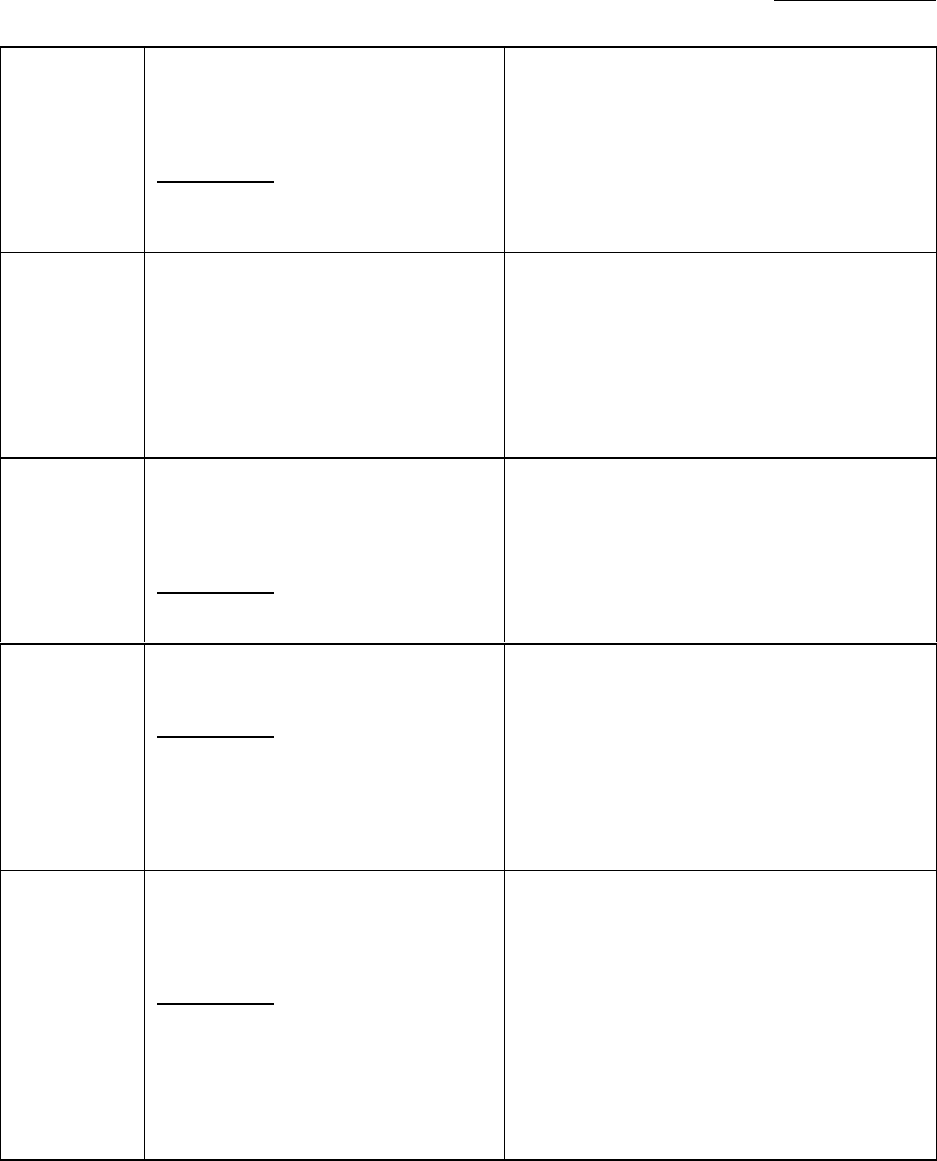

Exhibit 1-1 (1 of 5)

REHABILITATION TAX CREDIT CHECK SHEET

Chapter 3 CERTIFIED HISTORIC

REHABILITATION CREDIT

PRIOR TO TRA 86 - 25 percent

TRA 86 CREDIT - 20 percent

**Also Note Transition Rules

Treas. Reg. § 1.48-12(a)

Applicable Law:

IRC § 47(a) (2)

IRC § 47(c) (2) (B) & (C)

IRC § 47(c) (3)

Treas. Reg. § 1.48-12(d)

Treas. Reg. § 1.48-12(d) (7) (i)

Treas. Reg. § 1.48-12(d) (7) (ii)

Treas. Reg. § 1.48-12(d) (2) to (6)

Anderson Case

Dennis Case

Girgis Case

*Prior to 1991:

IRC § 48(g) contains similar provisions

Two certifications are necessary:

Certification of the Structure

Must be a “Certified Structure” or located in a

historical district and contribute to the significance

of the district. This is only a prerequisite to

potentially qualify for the rehabilitation credit as

outlined below.

Certification of the Rehabilitation

Additionally, the rehabilitation must be a “Certified

Rehabilitation” as certified by the Dept. of

Interior/National Park Service. Must have an

approved Part III certification from the NPS. Note,

review of the Parts I, II and III applications along

with the project folder at the National Park Service

can be helpful to develop and support many issues.

NOTE: If a project lacks certification from the NPS, the

credit should be disallowed in the year taken. Also

note that a position has been developed that can be

used on cases lacking certification even if the 3

year statute is barred. This position will be

supported by Chief Counsel. See Chapter 3.

Chapter 4 NON-HISTORIC CREDIT

Prior to TRA 86 -

20 percent CREDIT (40 YR BLDG)

15 percent CREDIT (30 YR BLDG)

TRA 86 - 10 percent CREDIT

** Also Note Transition Rules

Treas. Reg § 1.48-12 (a)

Applicable Law:

IRC § 47 (a) (1)

IRC § 47(c) (1)

IRC § 47(c) (2) (B) & (C)

Treas. Reg. § 1.48-12(d) (1) to (6)

Treas. Reg. § 1.48-12(c) (7) (iv)

Treas. Reg. § 1.48-12(b) (3) to (5)

Bailey Case

Depot Investors Case

Girgis Case

Nalle Case

*Prior to 1991:

IRC § 48(g) contains similar provisions.

Prior to TRA 86, Non-historic Credits were as follows:

For 20 percent credit, Must be 40 year old bldg.

For 15 percent credit, Must be 30 year old bldg.

Non-historic credit after TRA 86 changes:

Under TRA 86 the building must have been originally

built before 1936.

Certification by the Dept. of the Interior is not required.

NOTE: If the property is in a certified historic district,

then it must receive DECERTIFICATION from

the Dept. of the Interior that the building is not

of significance to the district. If NO

decertification, then no credit is allowable.

Also, Non-historic credits may not be taken for

buildings separately listed on the National

Register.

Decertification was required both before and after TRA

86. Treas. Reg. § 1.48-12(c) (7) (iv).

NOTE: Non-historic credits are not available for

buildings which are residential rental.

NOTE: Wall retention requirements apply to non-

historic rehabs after TRA 86 and all rehabs

prior to TRA 86.

1-5 3149-109

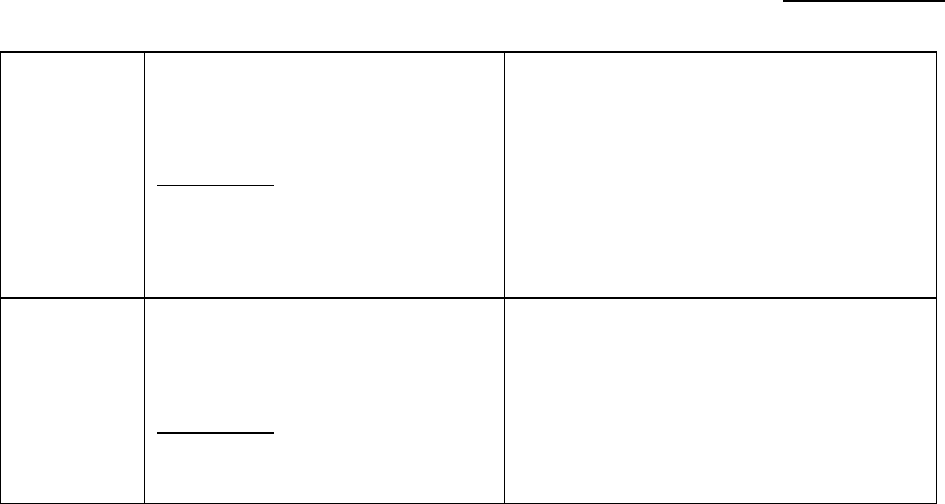

Exhibit 1-1 (2 of 5)

Chapter 5 PLACED IN SERVICE

**Applies both before and after TRA 86

Applicable Law:

IRC § 47(b)

Treas. Reg. § 1.48-12(f) (2)

Treas. Reg. § 1.48-12(c) ( 6)

Girgis Case

The rehab credit for qualified rehab expenditures is

generally allowed in the taxable year in which the

property is placed in service.

NOTE: The concept of “Placed in Service” can relate to

either the entire building or a portion of the

building which is completed and available for

rent or its respective income producing activity.

Chapter 6 SUBSTANTIAL REHABILITATION

**Applies both before and after TRA 86

Applicable Law:

IRC § 47(c) (1)

Treas. Reg. § 1.48-12(b) (1) & (2)

Alexander Case

** Also note section regarding multiple

buildings (“Site”).

In addition to receiving certification, projects must meet

a substantial rehabilitation test in order to qualify for the

credit.

The qualified rehabilitation expenditures during the 24

month period selected by the taxpayer must exceed the

greater of $5,000 or the adjusted basis of the property

determined at the beginning of such 24 month period.

NOTE: Special 60 month rule (if phased rehab) must be

part of architects plans, etc., IRC § 47(c)

(1)(c)(ii) & Treas. Reg. § 1.48-12(b) (1).

NOTE: Congress’ intent was that a substantial amount

of work was done and not just cosmetics. The

test is intended to quantify “substantial”. This

is one of the most confusing areas of Rehab

Law.

Chapter 7 BASIS REDUCTION

** Applies both before and after TRA 86 but

at different percent’s.

Applicable Law:

Treas. Reg. § 1.48-12(e)

Basis reduction required:

After TRA 86:

The basis of the rehab expenditures must be reduced by

100 percent of the credit as taken.

Before TRA 86:

The basis of the rehab expenditures must be reduced by

50 percent of the credit as taken. For Non-historic

projects, the basis reduction was increased to 100

percent for projects started after 1985.

Chapter 8 STRAIGHT LINE COST RECOVERY

**Required both before and after TRA 86.

Applicable Law:

IRC § 47(c) (2) (B) (I)

Treas. Reg. § 1.48-12(c) (7) (I)

Au Case

DeMarco Case

Manning Case

Straight Line Cost Recovery Required:

Before TRA 86:

-Incurred after 12/31/81: 15 yrs. S/L

-Incurred after 03/15/84: 18 yrs. S/L

-Incurred after 05/08/85: 19 yrs S/L

After TRA 86: (MACRS-Methods)

-Incurred after 12/31/86

Residential - 27.5 Yrs.

Non-Residential - 31.5 Yrs.

-Incurred after 5/12/93:

Residential = 27.5, Non-Residential = 39

Under the rehab provisions, there is a requirement that a

straight-line method of depreciation be used.

3149-109 1-6

Exhibit 1-1 (3 of 5)

Chapter 9 CREDIT RECAPTURE

** Required both before and after TRA 86

Applicable Law:

IRC § 50 (a)

Treas. Reg. § 1.48-12(f) (3)

Rome Case

*Prior to Rev Rec of 90

IRC § 47(a) contains similar provisions.

If there is a disposition or if the property ceases to be

ITC property before the close of the recapture period of

5 years, there is a recapture of the credit amounting to

20 percent of the credit taken for each year less than 5

full years.

NOTE: Although the credit is fully allowed in a given

year, as long as the property had been placed in

service by year end, the credit recapture is

based on a “Full Year” concept. It is necessary

to determine the actual date placed in service in

order to compute the recapture.

Chapter 10 ACQUISITION COSTS EXCLUDED

** Both before and after TRA 86.

Applicable Law:

IRC § 47(c) (2)(B)(ii)

Treas. Reg. § 1.48-12(c)(7)(ii)

Treas. Reg. § 1/48-12(d) (9)

Acquisition costs are specifically excluded from the

definition of qualified rehabilitation expenditures. The

cost of acquiring any building or interest, therein; pre-

rehab cost of acquiring the building or the cost of

acquiring a rehabilitation building that had previously

been placed in service would not qualify. Acquisition

costs are still included in the depreciable basis using the

straight method. Also see issue regarding developer’s

fees and other costs which could potentially be

recharacterized for their proper tax treatment.

Chapter 11 ENLARGEMENT EXPENDITURES AND

DEMOLITION EXCLUDED

** Both before and after TRA 86.

Applicable Law:

IRC § 47 (c)(2)(B)(iii)

Treas. Reg. § 1.48-12(c)(7)(iii)

Treas. Reg. § 1.48-12(d)(10)

IRC § 280B - Demolition

Enlargement costs of an existing building are

specifically excluded from the definition of qualified

rehabilitation expenditures. A building is enlarged to

the extent that total volume is increased. Enlargement

costs are still includible in the depreciable basis using

the straight line method. Enlargement costs should be

removed from the credit basis using a reasonable

method of allocation. Demolition costs qualify as long

as the building remains after the allowable demolition.

Chapter 12 SITEWORK EXPENDITURES EXCLUDED

** Applies both before and after TRA 86.

Applicable Law:

Treas. Reg. § 1.48-12(c) (5)

Sitework expenditures do not qualify for the credit and

should be removed from the credit basis. Sitework

includes any expenditures incurred for areas adjacent to

or related to the rehabilitated building including

sidewalks, paving, landscaping, parking lots, decks,

remote site lighting, fencing, railings, ornamental

fencing, gazebos, etc.

Chapter 13 SECTION 38/PERSONAL PROPERTY

EXCLUDED

** Applies both before and after TRA 86

Applicable Law:

IRC § 47(c) (2) (A)

IRC § 38

** See numerous court cases included in this

section

Regular IRC § 38 Investment Credit property does not

qualify for the rehab credit. Examples are office

equipment, furniture, carpeting, drapes, kitchen

appliances, cabinets, etc.

NOTE: If disallowing or removing Section 38 property

from the rehab basis then the straight line

recovery election is no longer required for those

items. Can allow ACRS, MACRS, etc.

The Rehab Credit is only for the building and its

structural components. There is sufficient law/cases

under the ITC sections to support.

1-7 3149-109

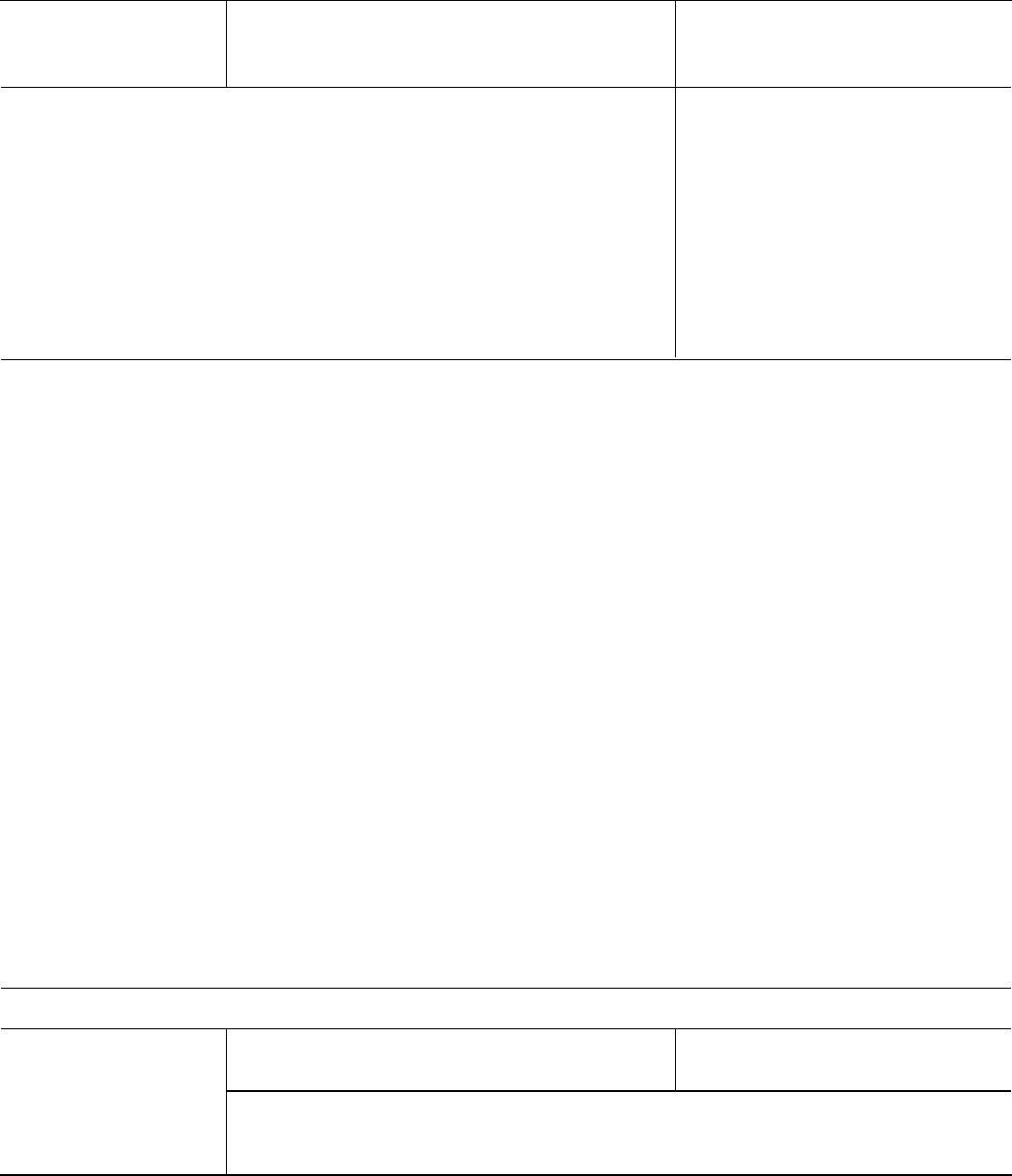

Exhibit 1-1 (4 of 5)

Chapter 14

TAX EXEMPT USE PROPERTY

EXCLUDED

Applicable Law:

IRC § 47(c) (2) (B) (v)

Treas. Reg. § 1.48-12(c) (7) (vi)

IRC § 168 (h)

Tax exempt use property is specifically excluded from

the definition of qualified rehabilitation expenditures.

Any expenditures allocated to the portion of the

property which is tax exempt use property must be

removed from the credit basis.

NOTE: There are special rules used to determine what

is tax exempt use property

Chapter 15 LESSEE EXPENDITURES

** Applies both before and after TRA 86.

IRC § 47(c) (2)(B)(vi)

IRC § 168(c)

Treas. Reg. § 1.48-12(c)(7)(v)

Eubanks Case

Lessees are permitted to qualify their leasehold

improvements incurred after 12/31/81 which otherwise

qualify as rehab expenditures for the credit as long as

the remaining term of the lease (without renewal

periods) is less than the recovery period as defined in

IRC § 168(c). (27.5 yrs for residential and 39 yrs for

non-residential real property).

NOTE: Lessees are also subject to the other issues

previously mentioned.

Chapter 16 CONSTRUCTION PERIOD INTEREST

AND TAXES

** Applies both before and after TRA 86.

Applicable Law:

IRC § 266

Treas. Reg. § 1.48-12(d)(9)

Election under IRC § 266 for construction period

interest and taxes during the actual rehab qualifies for

the credit.

A statement of the election should be attached to the

original return.

Be sure to exclude any acquisition related interest from

the rehab basis.

Chapter 17 PROGRESS EXPENDITURES

Applicable Law:

IRC § 47(d)

Treas. Reg. § 1.48-12(f) (2)

*Prior to Rev Rec of 90 IRC § 46(d)

contains similar provisions

Usually, placed in service is the correct timing for

taking the credit. An election can also be made to take

credit corresponding to progress expenditures incurred

during a tax year. It is still necessary to meet the

requirements of the substantial rehabilitation test as

previously mentioned. There are also special provisions

of self-rehabilitated property

Chapter 18 FACADE EASEMENT REDUCTION OF

BASIS

Applicable Law:

Rev. Rul. 89-90

Rev. Rul. 64-205

Treas. Reg. § 1.170A-13(h) (3)(iii)

Rome Case

Note: Disregard any Letter Rulings to the

contrary

Reduction of basis of property retained should be

adjusted by the part of the basis allocable to the

easement granted. The method of determining the

reduction of basis regarding the donation of the

easement is to allocate the value of the easement to the

shell, land and building and thus to reduce the basis of

the rehab expenditures to the extent of disposition via

the contribution.

NOTE: If the building was rehabilitated and the credit

taken prior to contribution of the facade easement then a

recapture would be necessary based on the disposition

and as calculated according to Section 50(a).

3149-109 1-8

Exhibit 1-1 (5 of 5)

Chapter 19 DEVELOPER FEE/DEVELOPMENT

COSTS

** Applies both before and after TRA 86.

Applicable Law:

** See Phila. District Developers Fee Brief

Carp/Zuckerman Case

Since the inception of the Rehabilitation Credit, “soft

costs” such as architectural and engineering fees,

consulting fees, site survey fees and “developer’s fees”

have always been allowable as part of the “Qualified

Rehab Basis”. As the term “developer’s fees” has never

been “quantified or qualified”, this remains a “gray

area” and has been discovered as a major area of abuse

for these type cases. Issues addressed include non-

allowable developer’s profit included in a purchase

price, disguised syndication fees, or amortizable costs,

and non-arm’s length transactions.

Chapter 23 PASSIVE ACTIVITY CREDIT

RESTRICTIONS

** Applies after TRA 86.

Applicable Law:

See Sidell vs. Commissioner

IRC § 469

Treas. Reg. § 1.469-1T

If the activity of the project is rental or is a non-rental

activity in which the owner/investor does not materially

participate, the passive activity rules will set limits on

the amount of credit that can be taken. Individuals can

offset credit not exceeding $7,000 ($25,000 X 28% tax

bracket) against their regular tax liability. The credit is

phased out for individuals with income of $200,000 to

$250,000.

1-9 3149-109

This page left intentionally blank.

3149-109 1-10

Chapter 2

CERTIFICATION PROCESS

The owner of a rehabilitated building can claim a rehabilitation tax credit as long as

three conditions are met. The building must have been substantially rehabilitated, it

must have been placed in service as a building before the beginning of the

rehabilitation work, and must be considered a certified historic structure. The term

“certified historic structure” is defined by IRC section 47(c)(3)(A). It is defined as

any building (and its structural components) which is either (a) listed in the National

Register, or (b) located in a registered historic district and is certified by the Secretary

of the Interior to the Secretary of the Treasury as being of historic significance to the

district.

The rehabilitation of a certified historic structure must meet the Department of the

Interior's standards for rehabilitation to qualify rehabilitation expenditures for the

rehabilitation credit. If the building or site is not separately listed, the owner can

apply to the Department of the Interior's National Park Service for an Evaluation of

Significance. This is done by filing Historic Preservation Certification Application

Part 1 - Evaluation of Significance (Form 10-168). This certification is not needed

for the non-historic credit.

Part 1 is used for the following purposes:

To request certification that a building contributes to the significance of a registered

historic district.

To request certification that a building or structure, and where appropriate, the land

area on which such building or structure is located contributes to the significance of a

registered historic district for charitable contribution for conservation purposes.

To request certification that the building does not contribute to the significance of a

registered historic district (needed to claim the non-historic rehabilitation credit, see

Chapter 4, Non-Historic Credits).

To request a preliminary determination whether an individual listing not yet on the

National Register meets the National Register Criteria for Evaluation and will likely

be listed in the National Register when nominated.

To request a preliminary determination that a building located within a potential

historic district contributes to the significance of the district.

To request a preliminary determination that a building outside the period or area of

significance of a registered historic district contributes to the significance of the

district.

2-1 3149-109

The application must include a description of the physical appearance of each

building, including all major features of the building, a statement of significance, and

photographs and maps.

All applications for preliminary determinations must contain all documentation

showing that the building, or the district where the building is located, meets the

National Register Criteria for Evaluation.

Historic Preservation Certification Application – Part 2 (Description of Evaluation

Form 10-168a) - must be completed by all owners of Historic Structures seeking to

have rehabilitation certified by the Secretary of the Interior. This form should be

completed and submitted prior to the initiation of any rehabilitation work. Proposed

work, which does not appear to be consistent with the Department of the Interior's

standards, will be identified. The owner will also be advised how to bring the project

into conformance with the Standards for Rehabilitation.

The application should include: name of the property; relevant data on existing

property; a detailed description of all the rehabilitation work, including all site work,

exterior and interior work, and new construction; internal and external "before"

photographs; drawing or sketches for plan alterations or new construction; and any

other special rehabilitation concerns. Examples of special rehabilitation concerns

may include storefront alterations; new heating, ventilation, or air conditioning

systems; windows; interior partitions and removing interior plaster; masonry

restoration; and new additions and new construction.

Once the rehabilitation work is completed, the owner must then submit a Request for

Certification of Completed Work (Form 10-168c). This form is often referred to as

Part 3. Part 3 must provide: completion date; signed statement by the owner(s)

expressing their opinion that the project meets the standards and it is consistent with

the work described in part 2; include costs and photographs of the completed work.

In addition, the names and taxpayer identification numbers of all the owners must be

provided. The overall project does not become a certified rehabilitation until the Part

3 is completed and approved by the National Park Service, and the building is

designated a "Certified Historic Structure."

A Representative of the Interior Department may inspect the completed work to see if

it meets the Standards for Rehabilitation. The Secretary of the Interior reserves the

right to make inspections at any time, up to 5 years after completion of the

rehabilitation, and to withdraw certification. A certification can be withdrawn if it is

found that the rehabilitation was not undertaken as presented by the owner in the

application and supporting documentation or that the owner made unapproved

additional alterations inconsistent with the Standards. Prior to the certification being

withdrawn, the owner is given 30 days to comment.

All completed application parts are sent to the State Historic Preservation Office

(SHPO). The SHPO will forward the applications to the appropriate National Park

Service Regional Office, generally with a recommendation. Parts 1 and 2 of the

application will generally be reviewed within 60 days (30 days at the State level and

30 days at the Federal level). The National Park Service will make notification as to

3149-109 2-2

certification in writing. A copy of each notification is provided to the Internal

Revenue Service and the SHPO.

A nonrefundable processing fee is charged for review of all Part 2 applications. Final

action will not be taken on an application until payment is received.

The final certification of both the structure and the rehabilitation work is not

necessary at the time the credit is taken. However, the certification must ultimately

be obtained by the building owners/taxpayers.

The certification of the structure and the rehabilitation work should be filed with the

return on which the credit was taken (Tax Form 3468 Investment Tax Credit). If the

final certification has not been obtained, then Parts 1 and 2 (as filed with the State

Historic Preservation Office) should be attached to Form 3468 indicating that the

National Park Service or the applicable State Historic Preservation Office received it.

There are additional requirements if a taxpayer does not obtain certification within 30

months of filing the tax return on which the Rehabilitation Tax Credit is claimed

(30-Month Rule). (Refer to Chapter 3, Certification Requirements, for detailed

explanation.)

Exhibit 2-1 National Park Service, Technical Preservation Services

Exhibit 2-2 is a listing of the State Historic Preservation Offices.

2-3 3149-109

This page left intentionally blank.

3149-109 2-4

This page left intentionally blank.

3149-109 2-6

Exhibit 2-2 (1 of 10)

STATE HISTORIC PRESERVATION OFFICES

Alabama: State Historic Preservation Officer

Alabama Historical Commission

468 South Perry Street

Montgomery, Alabama 36130-0900

334-242-3184

Alaska: State Historic Preservation Officer

Department of Natural Resources

Division of Parks and Outdoor Recreation

550 W 7th Avenue, Suite 1310

Anchorage, Alaska 99501-3565

907-269-8715

American Samoa: Territorial Historic Preservation Officer

American Samoa Historic Preservation Office

American Samoa Government

Pago Pago, American Samoa 96799

684-633-2384

Arizona: State Historic Preservation Officer

Office of Historic Preservation

Arizona State Parks

1300 W. Washington

Phoenix, Arizona 85007

602-542-4009

Arkansas: State Historic Preservation Officer

Arkansas Historic Preservation Program

1500 Tower Building

323 Center Street

Little Rock, Arkansas 72201

501-324-9880

2-7 3149-109

California:

Colorado:

Connecticut:

Delaware:

District of Columbia:

Florida:

Exhibit 2-2 (2 of 10)

State Historic Preservation Officer

Office of Historic Preservation

Department of Parks and Recreation

P.O. Box 942896

Sacramento, California 94296-0001

916-653-6624

State Historic Preservation Officer

Colorado History Museum

1300 Broadway

Denver, Colorado 80203-2137

303-866-3355

State Historic Preservation Officer

Connecticut Historical Commission

59 South Prospect Street

Hartford, Connecticut 06106

860-566-3005

State Historic Preservation Officer

Division of Historical and Cultural Affairs

Hall Of Records

P.O. Box 1401

Dover, Delaware 19901

302-739-5313

State Historic Preservation Officer

D.C. Financial and Control Board

941 No. Capitol Street NE

Room 2100

Washington, D.C. 20002

202-442-4570

State Historic Preservation Officer

Division of Historical Resources

R.A. Gray Building

500 S. Bronough Street

Tallahassee, Florida 32399-0250

850-488-1480

3149-109 2-8

Exhibit 2-2 (3 of 10)

Georgia: Commissioner

Department of Natural Resources

205 Butler Street, SE.

Atlanta, Georgia 30334

404-656-3500

Guam: Acting Historic Preservation Officer

Department of Parks and Recreation

Division of Historic Resources

P.O. Box 2950

Agana Heights, Guam 96910

671-475-6290

Hawaii: State Historic Preservation Officer

Department of Land and Natural Resources

1151 Punchbowl Street

Honolulu, Hawaii 96813

808-548-6550

Idaho: Director

State Historic Preservation Office

210 Main Street

Boise, Idaho 83702-7264

208-334-3890

Illinois: State Historic Preservation Officer

Illinois Historic Preservation Agency

Preservation Services Division

One Old State Capitol Plaza

Springfield, Illinois 62701

217-785-9045

Indiana: State Historic Preservation Officer

Department of Natural Resources

402 W. Washington Street

Room W 274

Indianapolis, Indiana 46204

317-232-4020

2-9 3149-109

Exhibit 2-2 (4 of 10)

Iowa: State Historic Preservation Officer

State Historical Society of Iowa

600 East Locust Street

Des Moines, Iowa 50319-0290

515-281-8837

Kansas: State Historic Preservation Officer

Kansas State Historical Society

Cultural Resources Division

6425 Southwest 6th Avenue

Topeka, Kansas 66615-1099

785-272-8681

Kentucky: State Historic Preservation Officer

Kentucky Heritage Council

300 Washington Street

Frankfort, Kentucky 40601

502-564-7005

Louisiana: State Historic Preservation Officer

Office of Cultural Development

P.O. Box 44247

Baton Rouge, Louisiana 70804

225-342-8160

Maine: State Historic Preservation Officer

Maine Historic Preservation Commission

55 Capitol Street

Station 65

Augusta, Maine 04333-0065

207-287-2132

Mariana Islands: State Historic Preservation Officer

Department of Community and Cultural Affairs

Northern Mariana Islands

Saipan, Mariana Islands 96950

670-664-2120

3149-109 2-10

Exhibit 2-2 (5 of 10)

Marshall Islands: State Historic Preservation Officer

Republic of the Marshall Islands

P.O. Box 1454

Majuro, Marshall Islands 96960

692-625-4642

Maryland: State Historic Preservation Officer

Department of Housing and Community Development

Peoples Resource Center

100 Community Place, 3rd floor

Crownsville, Maryland 21032-2023

410-514-7600

Massachusetts: State Historic Preservation Officer

Massachusetts Historical Commission

Massachusetts Archives Facility

220 Morrissey Boulevard

Boston, Massachusetts 02125

617-727-8470

Michigan: State Historic Preservation Officer

Bureau of Michigan History

Department of State

717 W. Allegan

Lansing, Michigan 48918-0001

517-373-0511

Minnesota: State Historic Preservation Officer

Minnesota Historical Society

State Historic Preservation Office

345 Kellogg Boulevard West

St. Paul, Minnesota 55102

651-296-2747

Mississippi: State Historic Preservation Officer

Mississippi Department of Archives and History

P.O. 571

Jackson, Mississippi 39205

601-359-6850

2-11 3149-109

Exhibit 2-2 (6 of 10)

Missouri: State Historic Preservation Officer

Department of Natural Resources

P.O. Box 176

Jefferson City, Missouri 65102

573-751-4732

Montana: State Historic Preservation Officer

Montana Historical Society

1410 8th Avenue

P.O. Box 201202

Helena, Montana 59620-1202

406-444-7715

Nebraska: State Historic Preservation Officer

Nebraska State Historical Society

1500 R Street

P.O. Box 82554

Lincoln, Nebraska 68501

402-471-4746

Nevada: State Historic Preservation Officer

Department of Museums, Library and Arts

100 No. Stewart Street

Capitol Complex

Carson City, Nevada 89701-4285

775-684-3440

New Hampshire: State Historic Preservation Officer

Division of Historical Resources

P.O. Box 2043

Concord, New Hampshire 03302-2043

603-271-6435

New Jersey: State Historic Preservation Officer

Department of Environmental Protection

CN-402

401 East State Street

Trenton, New Jersey 08625

609-292-2885

3149-109 2-12

Exhibit 2-2 (7 of 10)

New Mexico: Acting Director

Office of Cultural Affairs

Villa Rivera Building, 3rd Floor

228 E. Palace Avenue

Santa Fe, New Mexico 87503

505-827-6320

New York: State Historic Preservation Officer

Office of Parks, Recreation and Historic Pres.

Empire State Plaza

Agency Building 1, 20th Floor

Albany, New York 12238

518-474-0443

North Carolina: State Historic Preservation Officer

Department of Cultural Resources

Division of Archives and History

4617 Mail Service Center

Raleigh, North Carolina 27699-4617

919-733-7305

North Dakota: State Historic Preservation Officer

State Historical Society of North Dakota

ND Heritage Center

612 East Boulevard Avenue

Bismarck, North Dakota 58505-0830

701-328-2672

Ohio: State Historic Preservation Officer

Ohio Historic Preservation Office

Ohio Historical Society

567 E. Hudson Street

Columbus, Ohio 43211-1030

614-297-2470

Oklahoma: State Historic Preservation Officer

Oklahoma Historical Society

Wiley Post Historical Building

2100 N. Lincoln Boulevard

Oklahoma City, Oklahoma 73105

405-521-2491

2-13 3149-109

Oregon:

Palau:

Pennsylvania:

Pohnpei State F.M.:

Puerto Rico:

Rhode Island:

Exhibit 2-2 (8 of 10)

State Historic Preservation Officer

Oregon Parks and Recreation Department

1115 Commercial Street N.E.

Salem, Oregon 97310-1001

503-378-5019

Historic Preservation Officer

Ministry of Social Services

Division of Cultural Affairs

P.O. Box 100, Government of Palau

Koror, Palau 96940

680-488-2489

State Historic Preservation Officer

Pennsylvania Historical and Museum Commission

P.O. Box 1026

Harrisburg, Pennsylvania 17108-1026

717-787-2891

Historic Preservation Officer

Dept. of Health, Education & Social Affairs

FSM National Government

P.O. Box PS 70

Palikir, Pohnpei State FM 96941

691-320-2343

State Historic Preservation Officer

La Fortaleza

P.O. Box 82

San Juan, Puerto Rico 00901

787-721-2676

State Historic Preservation Officer

Hist. Preservation and Heritage Commission

Old State House

150 Benefit Street

Providence, Rhode Island 02903

401-222-2678

3149-109 2-14

Exhibit 2-2 (9 of 10)

South Carolina: State Historic Preservation Officer

Department of Archives and History

8301 Parklane Road

Columbia, South Carolina 29223-4905

803-896-6100

South Dakota: State Historic Preservation Officer

South Dakota State Historical Society

900 Governors Drive

Pierre, South Dakota 57501-2217

605-773-3458

Tennessee: State Historic Preservation Officer

Department of Environment and Conservation

2941 Lebanon Road

Nashville, Tennessee 37243-0442

615-532-0109

Texas: State Historic Preservation Officer

Texas Historical Commission

P.O. Box 12276

Capitol Station

Austin, Texas 78711-2276

512-463-6100

Utah: State Historic Preservation Officer

Utah State Historical Society

300 Rio Grande

Salt Lake City, Utah 84101

801-533-3551

Vermont: State Historic Preservation Officer

Agency of Commerce & Community Development

VT Division for Hist. Preservation

National Life Bldg., Drawer 20

Montpelier, Vermont 05620-0501

802-828-3056

2-15 3149-109

Exhibit 2-2 (10 of 10)

Virginia: State Historic Preservation Officer

Department of Historic Resources

2801 Kensington Avenue

Richmond, Virginia 23221

804-367-2323

Virgin Islands: State Historic Preservation Officer

Dept. of Planning & Natural Resources

Nisky Center, Suite 231

No. 45A Estate Nisky

St. Thomas, Virgin Islands 00803

340-776-8605

Washington: State Historic Preservation Officer

Office of Archeology & Historic Preservation

Commerce, Trade & Econ. Dev.

420 Golf Club Road S.E., Suite 201

Lacey, Washington 98504-1048

360-407-0765

West Virginia: State Historic Preservation Officer

Division of Culture and History

1900 Kanawha Boulevard E.

Capitol Complex

Charleston, West Virginia 25305

304-558-0220

Wisconsin: State Historic Preservation Officer

State Historical Society

816 State Street

Madison, Wisconsin 53706

608-264-6500

Wyoming: State Historic Preservation Officer

Wyoming State Historic Preservation Office

Dept. of State Parks & Cultural Resources

2301 Central Avenue, Barrett Bldg., 3rd floor

Cheyenne, Wyoming 82002

307-777-7697

3149-109 2-16

Chapter 3

CERTIFICATION REQUIREMENTS

BACKGROUND

To obtain the 20 percent Certified Historic Rehabilitation Credit the property must

either be listed on the National Register of Historic Places or located in a Registered

Historical District and be determined "significant" to that district. Additionally, the

Secretary of the Interior must certify to the Secretary of the Treasury that the project

meets their "standards" and is a "Certified Rehabilitation." The owner obtains this

certification by filing the three-part application with the National Park Service.

To have work on a rehabilitation project certified by the National Park Service, there

are a series of applications that are filed with the appropriate State Historic

Preservation Office (SHPO). These applications are reviewed and then forwarded,

with recommendations by the SHPO, to the National Park Service for approval or

denial. The applications include:

Part 1 - Evaluation of Significance - This part should contain a narrative that

describes the history of the particular building and the present condition of

the building. This part should also include a summary as to how the

building contributes to the significance of the historical district within which

it is located.

Part 2 - Description of Rehabilitation - This part is intended to provide both the

State Historic Preservation Office and the National Park Service with a

narrative describing proposed rehabilitation work. The owners should also

include photographs to document the particular architectural and historical

features of the building as they currently exist.

Note: It is usually recommended that both Part 1 and 2 are filed before any work is

started on the project.

Part 3 - Request for Certification of Completed Work - This final part of the

application process is intended to be filed by the owners to notify both the

State Historic Preservation Office and the National Park Service that the

project is completed. By filing the final part, the owners are requesting that

the project be reviewed to receive certification. This part includes

photographs of the completed rehabilitation project. In some cases, an

authorized representative of the Secretary may inspect the completed project

to determine if the work meets the “Standards for Rehabilitation”.

When examining a return exhibiting the Historic Rehabilitation Credit, it is necessary

(at a minimum) to verify:

3-1 3149-109

1. the project has received "certification" of the work, and

2. the building was deemed a "Certified Historic Structure" by virtue of either

a. being separately listed in the National Register of Historic Places, or

b. by its location in a registered historic district and the determination that it

“contributes to the significance" of that district.

This certification of both the structure and the rehabilitation work is not necessary at

the time that the credit is taken. Ultimately, however, the certification must be

obtained by the building owners/taxpayers. Under Treasury Regulation section

1.48-12(d)(7)(i) and (ii), it is indicated that the certification should be filed with the

return on which the credit was taken. If final certification has been obtained, the

owner must submit a copy of the Part 3 certification as an attachment to Form 3468

with the first income tax return filed after certification is received. If the final

certification has not been obtained, then Parts 1 and 2 (as filed with the State Historic

Preservation Office) should be attached to Form 3468 indicating that the National Park

Service or the applicable State Historic Preservation Office received it.

(Please note: Form 3468 is in the process of being revised to accommodate

electronic filers. This revision may no longer require attaching Part 3 to Form

3468. Part 3 information, however, may be obtained from the State Historic

Preservation Office or the National Park Service.)

Treas. Reg. section 1.48-12(f )(2), states that the credit may be claimed if the property

is placed in service, and the substantial rehabilitation test has been met. The pro forma

Information Document Request (Form 4564) addresses this issue based on the request

of items number 2, 5, 6, and 15. (See Exhibit 3-1.) Treas. Reg. section 1.48-

12(d)(7)(ii) lists the steps prescribed for dealing with late certifications. Included with

this section is a "30 Month Rule" which indicates that if the taxpayer fails to receive

final certification of completed work prior to the date that is 30 months after the date

that the taxpayer filed the tax return on which the credit was claimed, the taxpayer

must submit a written statement to the district director stating such fact prior to the last

day of the 30

th

month, and the taxpayer should be requested to consent to an agreement

under IRC section 6501(c)(4) extending the period of assessment for any tax relating

to the time for which the credit was claimed.

Based on the above, and legal arguments including the "Doctrine of Equitable

Estoppel," examiners in conjunction with the offices of District Counsel, and Chief

Counsel, have developed a position for dealing with cases where the normal 3-year

statute of limitations is barred. This position has been applied to cases where the

proper certification was never obtained, and where the 30 month rule as cited above

was ignored. These cases can be completely developed based on documentation from

the National Park Service.

If the final certification was not obtained, and an examiner has a case either within

statute, or where the statute is barred, that taxpayer/owner should be notified, and

afforded one last opportunity to obtain the proper certification from the National Park

Service. If the certification is denied, and all avenues of attaining the certification

3149-109 3-2

have been exhausted, then the credit should be disallowed in the year taken. Lack of

certification does not constitute a credit recapture under IRC section 50(a), or

previously under IRC section 47(a), but in fact should be disallowed in the year taken

based on the law sections which follow.

Also note that the estoppel position can only be used in cases where IRS becomes

aware of the lack of certification after the normal 3-year statute has expired. If you are

examining a tax return that exhibits an historic credit, and you have determined that

the subject building lacks the necessary certification, you should ensure that the statute

is protected until the final certification is obtained, or the credit has been properly

disallowed. If an examiner discovers that they have a case lacking certification where

the statute is barred, and the estoppel position may be applied, they should contact

their District Counsel.

LATE SUBMISSION OF THE HISTORIC PRESERVATION

CERTIFICATION APPLICATION

Chapter 2 Treas. Reg. section 1.48-12(d)(1) and 1.48-12(d)(7) deals directly with the

late submission of Parts 1, 2 and 3 of the “Historic Preservation Certification

Application” and how late submission may prevent a taxpayer from claiming the

rehabilitation tax credit.

To better understand the consequences that result from the late submission of Parts 1,

2, and 3 of the “Historic Preservation Certification Application”, it is important to

review the pertinent sections of the Treasury Regulations and the Internal Revenue

Code.

IRC section 47(b) indicates that the credit should be claimed when the building is

placed in service. It specifically provides that “qualified rehabilitation expenditures,

with respect to any qualified rehabilitated building, shall be taken in to account for the

taxable year in which such qualified rehabilitated building is placed in service.”

Treas. Reg. section 1.48(f)(2) reiterates the fact that the credit is claimed when the

property is placed in service, and adds the language “meets the definition of a qualified

rehabilitated building for the taxable year.” This special language means that, in

addition to the placed in service provision, the building owner must also meet the

substantial rehabilitation test for that year.

LATE SUBMISSION OF PART 1

To be eligible for the 20 percent rehabilitation tax credit, the property must also be a

certified historic structure. Treas. Reg. section 1.48-12(d)(1) provides rules relating to

the rehabilitation of certified historic structures. A certified historic structure is

defined in this regulation as “any building and its structural components that is listed

in the National Register of Historic Places or located in a registered historic district

and certified by the Secretary of Interior as being of historic significance to the district.

3-3 3149-109

For purposes of this section, a building shall be considered to be a certified historic

structure at the time it is placed in service if the taxpayer reasonably believes on that

date the building will be determined to be a certified historic structure and has

requested on or before that date a determination from the Department of Interior

that such building is a certified historic structure within the meaning of this

paragraph and the Department of Interior later determines that the building is a

certified historic structure.”

Simply stated, Treas. Reg. section 1.48(d)(1) requires that the taxpayer submit Part 1

of the Historic Preservation Certification Application before the property is placed in

service.

The only exception where Part 1 would not have to be submitted prior to the placed in

service date would be if the building were already individually listed in the National

Register. If a building were listed in the National Register, the property owner would

have already requested a determination from the Department of Interior that the

building was a certified historic structure.

It is important to note that a building that is simply located in a registered historic

district would not fall under this exception. This is true even if the building was

specifically listed as one of the contributing buildings in the registered historic district

nomination.

LATE SUBMISSION OF PART 3

Treas. Reg. section 1.48-12(d)(7) and (f)(2) indicate that if the property is placed in

service and the taxpayer reasonably expects that the National Park Service will

approve Part 3 of the “Historic Preservation Certification Application”, Certification

of Completed Work, the tax credit can be claimed by the taxpayer. If the taxpayer,

however, fails to receive the final certification of completed work within 30 months

after filing the tax return on which the credit was claimed, the taxpayer must submit a

written statement to the Internal Revenue Service stating such fact prior to the last day

of the 30

th

month. In such case the taxpayer will be requested to extend the normal 3-

year statute of limitation period for the return on which the credit was claimed.

If the taxpayer claims the rehabilitation tax credit, but never receives Part 3 approval

from the National Park Service, the taxpayer must recapture the entire credit.

A taxpayer does not have a “certified rehabilitation” until it receives a Part 3 approval.

In other words, the taxpayer is not entitled to the rehabilitation tax credit unless the

Department of the Interior has certified the rehabilitation project by signing Part 3 of

the “Historic Preservation Certification Application”. The definition of the term

“certified rehabilitation” is found in Treas. Reg. section 1.48-12(d)(3).

Treas. Reg. section 1.48-12(d)(3) states that the term “certified rehabilitation” means

any rehabilitation of a certified historic structure that the Secretary of the Interior has

3149-109 3-4

certified to the Internal Revenue Service as being consistent with the historic character

of the building and, where applicable, the district in which such building is located.

STATUTE OF LIMITATIONS

In general, the statute of limitation is 3 years from the due date of the return. IRC

section 6511(a) provides that a claim for credit or refund of an overpayment of any tax

shall be filed by the taxpayer within 3 years from the time the return was filed or 2

years from the time the tax was paid, whichever the periods expire the later.

If a taxpayer placed a “certified rehabilitation” in service, but never claimed the

rehabilitation tax credit, the taxpayer would have 3 years from the due date of the

return filed for the year the property was placed in service, to file a claim for refund.

Once this period expires, the taxpayer will not be eligible to claim the rehabilitation

tax credit.

AUDIT TECHNIQUES

Determine if the building was listed in the National Register before the property was

placed in service. The State Historic Preservation Office will be able to provide this

information. If the taxpayer was only required to submit a Part 2 and 3 of the Historic

Preservation Certification Application, this would be an indication that the property is

already listed in the National Register and would fall under the exception to the rule

that Part 1 be submitted prior to the placed in service date.

Review Part 1 of the Historic Preservation Certification Application to determine

when it was submitted to the State Historic Preservation Office. If the building is

located in a historic district determine if Part 1 was submitted prior to the placed in

service date. If a determination is made that the Part 1 was not submitted before the

placed in service date, an adjustment should be made to recapture the entire credit.

CERTIFICATION LAW SECTIONS

IRC section 47(a) - Rehabilitation Credit/Amount of Credit

IRC section 47(b) - When the credit may be claimed.

Treas. Reg. section 1.48-12(f)(2) - When the credit may be claimed/if placed in service

and substantial rehabilitation test has been met.

IRC sections 47(c)(2)(B), 47(c)(2)(C) and 47(c)(3), and Treas. Reg. section 1.48-12(d)

- Certain expenditures are not included.

Treas. Reg. section 1.48-12(d)(7)(i) - Notice of certification required with return.

3-5 3149-109

Treas. Reg. section 1.48-12(d)(7)(ii) - Late Certification and 30-Month Rule.

Treas. Reg. section 1.48-12(d)(2) - Definition of Registered Historic District.

Treas. Reg. section 1.48-12(c)(7)(iv) - Non-certified rehabilitation is not allowable for

certified, historic structures (building separately listed on the National Register of

Historic Places) or for buildings located in a registered historic district (buildings

determined to be "significant to the district").

COURT CASES

In Girgis V. Commissioner, T.C. Memo 1991-191, a decision was entered that in

order for an expenditure in connection with the rehabilitation of a "Certified Historic

Structure" to be a "Qualified Rehabilitation Expenditure," the rehabilitation must be a

"Certified Rehabilitation" as defined under IRC section 48(g)(2)(B)(iv) (or under

current law 47(c)(2)(B)(iv)). It goes on further to define a "Certified Rehabilitation"

as "any rehabilitation of a certified historic structure which the Secretary of the Interior

has certified to the Secretary (of the Treasury) as being consistent with the historical

character of such property or the district in which such property is located," IRC

section 48(g)(2)(C) (or under current law 47(c)(2)(C)). It was also held that if a

building is deemed to be a "Certified Historic Structure", that building will only

qualify for the historic rehabilitation credit and does not qualify for the non-historic

credit for older buildings. The courts cited IRC sections 48(g)(1) and 46(b)(4)(C)(ii)

(under current law, sections 47(a)(1) and 47(c)(1)).

In B. G. Anderson, 62 TCM 1324, Dec. 47,769(M), T.C. Memo, 1991-583, no

rehabilitation tax credit was allowed based on the mere listing of a building on the

National and Philadelphia Register of Historic Places.

In Booker T. Washington Broadcasting Services Inc. v. United States, 92-2 U.S.T.C.

50,545, a taxpayer was not entitled to the certified rehabilitation tax credit because

taxpayer failed to apply for certification until nearly 3 years after taxpayer claimed the

credit.

In J. Franklin Dennis and Beverly A. Dennis v. Commissioner, T.C. Memo 1993-

345, a property owner was denied the rehabilitation tax credit because the owner used

the property solely as his personal residence. Further, he had not received a

certification of the rehabilitation from the Secretary of the Interior. Furthermore, there

was no evidence that the owner followed the "30 month rule."

In Schneider Partnership, DC N. J., 89-1 U.S.T.C. 9319, no rehabilitation tax credit

was allowed where the certification was denied by the Secretary of the Interior.

3149-109 3-6

Exhibit 3-1 (1 of 3)

Form 4564

Rev. 6/88

Department of the Treasury

Internal Revenue Service

INFORMATION DOCUMENT REQUEST

Request Number

TO: Name of Taxpayer and Co. Div. or Branch

Please return Part 2 with listed documents

to requester identified below.

Subject

_________________________

_

SAIN No.|Submitted to:

|

|

________|________________

_

Dates of Previous

Requests

Description of Documents Requested

Please present the following documents and information regarding the

partnership examination for tax year(s) __________________________.

1. A copy of the Prospectus/Offering Memorandum relating to the above partnership activity.

2. Certification of rehabilitation expenses by The Department of The Interior (Parts I, II, and III) if applicable.

a. Exact address or location of the building.

b. Does the above partnership own the entire rehabilitated structure. If not, please provide a statement indicating what

portion of the building the partnership owns.

____%; ____units of a total of____units; ____floors of a total of ____floors; etc.

Information Due By__________ At Next Appointment [ ] Mail In [ ]

Name and Title of Requester Date

FROM:

Office Location

3-7 3149-109

Exhibit 3-1 (2 of 3)

Form 4564

Rev. 6/88

Department of the Treasury

Internal Revenue Service

INFORMATION DOCUMENT REQUEST

Request Number

TO: Name of Taxpayer and Co. Div. or Branch

Please return Part 2 with listed documents

to requester identified below.

Subject

_________________________

_

SAIN No.|Submitted to:

|

|

________|________________

_

Dates of Previous

Requests

Description of Documents Requested

3. If the building is not a certified rehabilitation, then please provide the following information:

a. Exact address or location of the building.

b. Does the above partnership own the entire rehabilitated structure. If not, please provide a statement indicating what

portion of the building the partnership owns.

____%;____units of a total of ____units; ____floors of a total of ____floors; etc.

4. Settlement sheets for the acquisition of any properties relating to the form 1065 filed.

5. Certificate and/or Statement of Occupancy.

6. Copy of the first lease executed.

7. If a facade easement is involved, please provide the Deed and Appraisal of the facade easement.

8. A copy of the partnership Form 1065 for tax year(s)_________________.

9. Workpapers used in preparing the return.

10. Copies of any Partnership Agreements executed.

Information Due By__________ At Next Appointment [ ] Mail In [ ]

Name and Title of Requester Date

FROM:

Office Location

3149-109 3-8

Exhibit 3-1 (3 of 3)

Form 4564

Rev. 6/88

Department of the Treasury

Internal Revenue Service

INFORMATION DOCUMENT REQUEST

Request Number

TO: Name of Taxpayer and Co. Div. Or Branch

Please return Part 2 with listed documents

to requester identified below.

Subject

_________________________

_

SAIN No.|Submitted to:

|

|

________|________________

_

Dates of Previous

Requests

Description of Documents Requested

11. All bank statements and canceled checks for the Partnership.

12. Financing Agreements/Mortgages for all properties.

13. Construction contract including a specific breakdown of rehabilitation costs and any construction loan

agreements.

14. Ledger Account/AIA statements for the construction mortgage showing draws for work performed.

15. Identification of the partnership's 24 or 60 month measuring period for purposes of the substantial

rehabilitation provisions.

16. Documentation/Records pertaining to the capital contributions made by all of the partners, including all notes.

17. Records of all loans and repayments.

**************************************************************************************

Note: The above IDR should be modified for different types of owners including Corporations and

Individuals, and should also be expanded to address any other issues that the examiner determines

to warrant review. Some of the items should be deleted if not applicable, for example, the

question regarding the Facade could be deleted if no Facade Contribution was taken by the taxpayer

under audit. Also for example, if you were examining a corporate taxpayer then the Corporate

Minutes might be requested instead of a Partnership Offering Memorandum.

******************************************************************

Information Due By__________ At Next Appointment [ ] Mail In [ ]

Name and Title of Requester Date

FROM:

Office Location

3-9 3149-109

Chapter 4

NON-HISTORIC CREDITS

BACKGROUND

As discussed in Chapter 1, the Economic Recovery Tax Act of 1981 introduced two

tiers of non-historic rehabilitation tax credits - a 20 percent credit for buildings that

were at least 40 years old, and a 15 percent credit for buildings that were at least 30

years old. The Tax Reform Act of 1986 created a single credit for non-historic

rehabilitation projects that amounts to 10 percent provided the building had been

originally placed in service before 1936.

To obtain the 10 percent non-historic rehabilitation tax credit, the property must meet

certain criteria. A taxpayer cannot claim a 10 percent rehabilitation tax credit on a

building that is in the National Register of Historic Places or is located within a

Registered Historic District unless it has been certified by the National Park Service

as not contributing to the significance of the district. To request “decertification”, the

taxpayer should submit Part 1 of the Historic Preservation Certification Application.

If a building is not in the National Register, or if it is located in a Registered Historic

District but has been determined to be a non-contributing structure by the Department

of the Interior, a 10 percent rehabilitation tax credit may be utilized provided the

building:

? Was placed in service before 1936 [See Treas. Reg. section 1.48-12(b)(4)];

? Is used for non-residential rental purposes [See IRC section 50(b)(2)];

? Has not been physically moved [See Treas. Reg. section 1.48-12(b)(5)];

? Meets the following internal and external wall retention [See Treas. Reg. section

1.48-12(b)(3)]:

- 50 percent or more of the existing external walls are retained in place as

external walls,

- 75 percent or more of the existing external walls are retained in place as

internal or external walls,

- 75 percent or more of the existing internal structural framework is retained in

place.

4-1 3149-109

Buildings that are “certified historic structures” are precluded from taking the 10

percent non-historic tax – only the historic 20 percent credit would apply.

DECERTIFICATION PROCEDURES

If a building is located within a historic district, but is generally of a different age

than the time frame as reflected in that district, or for any other reason the building

does not contribute to, or is not characteristic of the historical integrity of that district,

the owner may apply to the National Park Service for "decertification."

Using the "Part 1" application, the owner submits a narrative to the State Historic

Preservation Office (and ultimately the National Park Service) to demonstrate that the

building, although physically located within the district, does not contribute to the

significance of the district.

NOTE: “Decertification” is the only way that the building owner would be entitled

to take the non-historic credit (assuming all other law provisions are followed). If a

case exhibiting a non-historic credit is encountered, the examiner should ensure that

the property is not separately listed, is not located within a historic district, or, if it is

located within a historic district, that the proper "decertification" was obtained in

order to qualify for the non-historic credit. As with the historic credits, if an

examiner encounters a case where a non-historic credit has been taken for property

located within a historic district, then the examiner should afford the building owner

the necessary time to obtain the "decertification." If the "decertification" cannot be

obtained, then the non-historic credit should be disallowed in full, unless the owner

can attain historic certification which would then qualify the building for the historic

rehabilitation credit. The State Historic Preservation Offices can usually provide

detailed maps of registered historic districts within the state.

The wall retention requirements previously existed for both the historic and the

non-historic credits prior to the Tax Reform Act of 1986, but were dropped for the

historic credits based on the practical implications. For certified projects, destruction

of walls, whether internal or external, must be approved by the National Park Service,

and is usually discouraged. The Code and regulations that follow address the

definitions and various technicalities of this section.

The pro forma Information Document Request (see Exhibit 3-1) addresses the

non-historic credit issue through the request of Item 3. The certification of the work

is not required for non-historic buildings as long as they are not considered "Certified

Historic Structures." It should also be noted that besides meeting the "use", "age,"

and "wall retention" requirements, it is also necessary to fulfill the other law

requirements such as the substantial rehabilitation test, use of straight-line

depreciation, etc.

3149-109 4-2

NON-HISTORIC CREDITS LAW

Rehabilitation Credit/Amount of Credit - See IRC section 47(a).

The prohibition of residential rental property for purposes of the credit exists for

non-historic credits but not those which qualify for the certified historic credit. See

Treas. Reg. section 1.48-1(h)(1)(i) and (h)(2)(iv).

For rules applicable to the rehabilitation of certified historic structures/certification

requirements refer to Treas. Reg. section 1-48-12(d).

Treas. Reg. section 1.48-12(d) provides the definition of a Registered Historic

District.

IRC section 47(c) - Definitions/Qualified Rehabilitated Building

IRC section 47(c)(1)(B) - Non-certified rehabilitation projects

Treas. Reg. section 1.48-12(b)(4) - Age Requirement/Non-certified rehabilitation

projects

Treas. Reg. section 1.48-12(b)(4)(ii) and (iii) - Effect of post-1936 building additions

and the effect of vacant periods for non-certified rehabilitation projects.

Treas. Reg. section 1.48-12(b)(5) - Building must not have been moved before 1936.

Treas. Reg. section 1.48-12(b)(6)(i) and (iii) – Definition and special rules for

“physical work” on a rehabilitation and adjoining buildings that were combined.

Wall Retention Requirements - IRC section 47(c)(1)(A), Treas. Reg. section 1.48-

12(b)(3)((i), Treas. Reg. section 1.48-12(b)(3)(i)(C) and (D), Treas. Reg. section

1.48-12(b)(3)(ii), Treas. Reg. section 1.48-12(b)(3)(iii), and Treas. Reg. section

1.48-12(b)(3)(iv), (v) and (vi).

COURT CASES

In Girgis V. Commissioner, T.C. Memo 1991-191, a decision was entered that if a

building is deemed to be a "Certified Historic Structure," that building will only

qualify for the historic rehabilitation credit, and does not qualify for the non-historic